U.S. natural gas prices will soon be set on the global stage

Teri Viswanath

Key points

- The long-held expectation of “stable, cheap, domestic” natural gas is reaching the end of its lifecycle. At the core of this shift is the growing role of LNG exports in U.S. price formation.

- A growing winter premium and sharper price swings for U.S. buyers are being driven not by local weather forecasts but by global LNG competition.

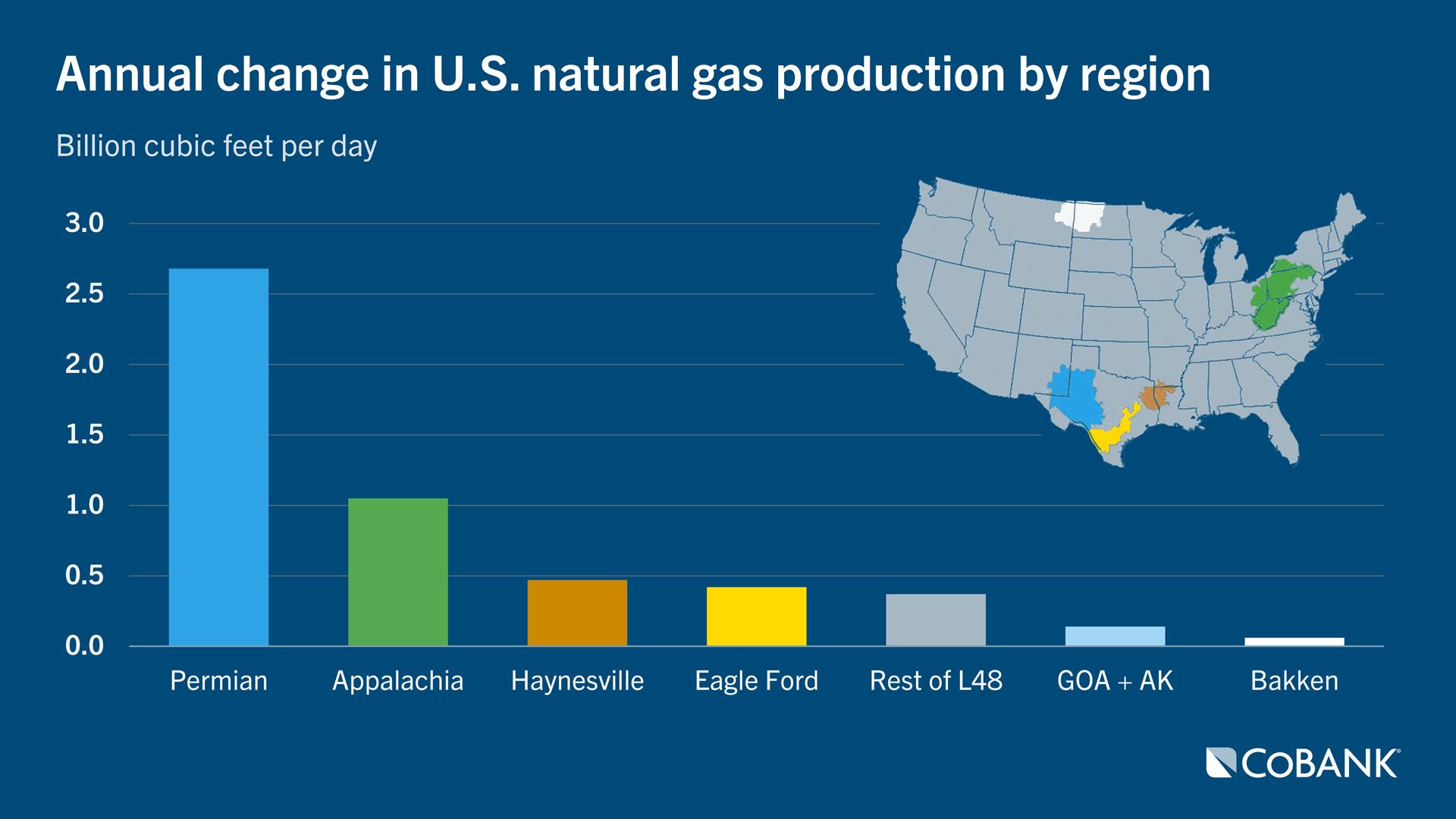

- Infrastructure is not adding certainty. Much of the recent pipeline buildout is designed to move gas toward LNG facilities rather than broadly rebalancing regional U.S. supply.

The U.S. natural gas market has entered a fundamentally different era — one defined by global integration, structurally higher price floors, and increased exposure to geopolitical and infrastructure risk. While domestic supply remains abundant, the forces shaping future U.S. prices will extend far beyond North American natural gas-directed production and weather. Liquefied natural gas (LNG) exports, geopolitical conflict, pipeline constraints, and oil linked supply dynamics are reshaping how prices form and how risk is transmitted across regions. For utilities and large gas consumers, the writing is on the wall — planning assumptions built around a stable, insulated, low price domestic gas market will soon be unreliable.

At the core of this shift is the growing role of LNG exports in domestic price formation. The United States has become the world’s largest LNG exporter, effectively importing global volatility into what was once a largely domestic market. Even though U.S. production currently exceeds domestic demand, higher global prices raise export netbacks, pulling gas toward LNG terminals and tightening the domestic balance. As a result, Henry Hub prices — the benchmark for North American natural-gas pricing — will be increasingly exposed at the margin to global demand rather than purely domestic fundamentals. This dynamic sets a price floor by shifting surpluses to exports when domestic prices fall but also raises the risk of greater volatility as export capacity expands and geopolitical events disrupt global supplies.

This structural change is evident in post 2022 price behavior. The extreme spikes of that year reflected acute scarcity and panic driven by global disruptions. Prices retreated in 2023 and early 2024 as U.S. production surged and storage rebuilt, but they did not return to the pre 2020 low price regime. Term pricing clearly reflects the fact that the market has reset to a higher trading range. Greater volatility will soon be apparent, but for now oscillates around a higher center of gravity, signaling that the era of $2 gas will soon be over. Moreover, geopolitical risk will be increasingly embedded into U.S. gas pricing, particularly during winter.

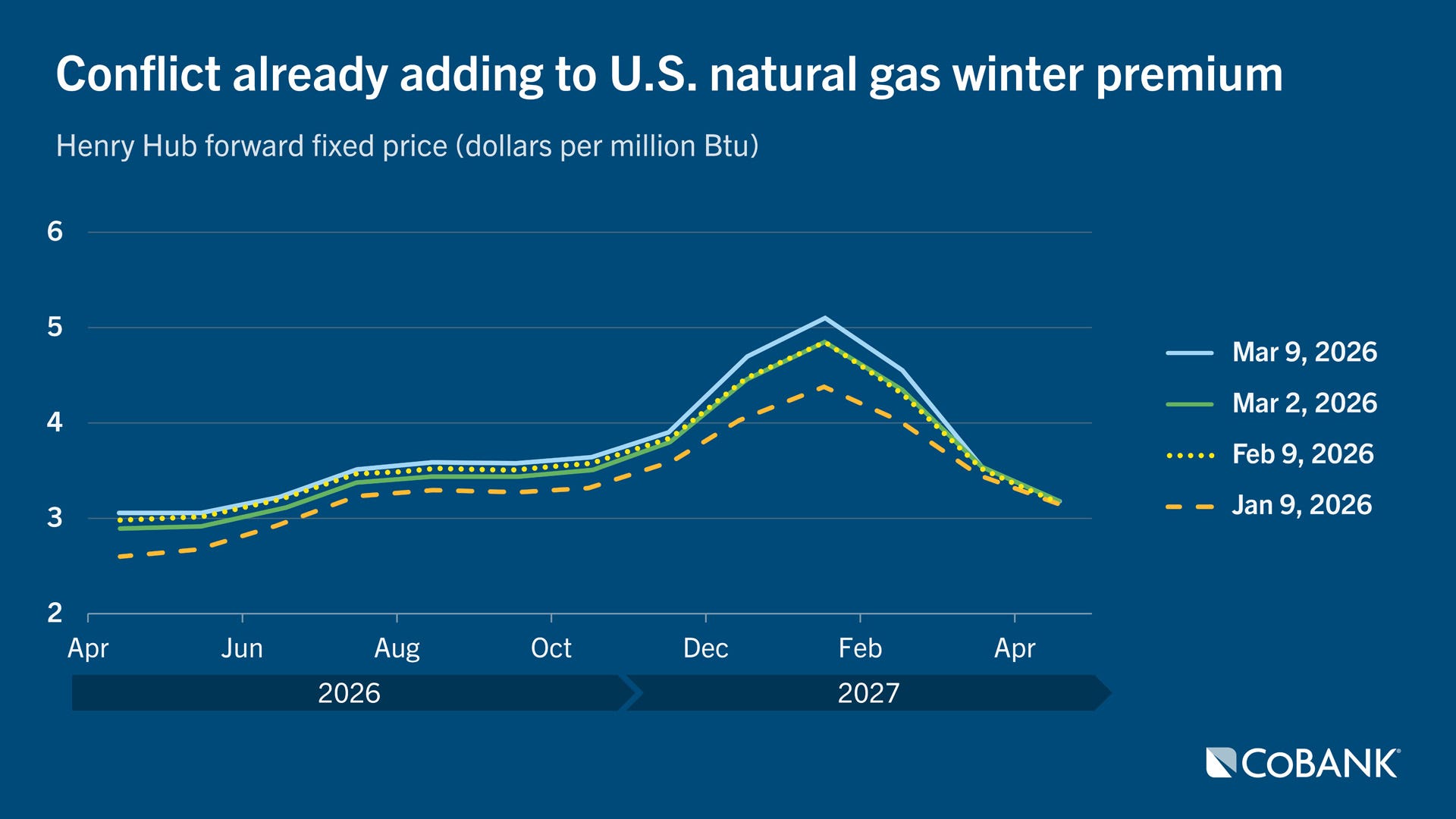

The current conflict in the Middle East has disrupted LNG flows through the Strait of Hormuz, a critical chokepoint for global LNG trade and a primary route for Qatari exports. The disruptions caused sharp spikes in Europe’s TTF (Title Transfer Facility) and JKM (Japan/Korea Marker), two of the three global LNG pricing benchmarks. And while Henry Hub, the third benchmark, remains slightly more shielded than West Texas Intermediate (the North American oil benchmark), Henry Hub now experiences “mood swings” as evidenced by the growing winter premium — driven not by local weather forecasts but by global LNG competition. For utilities, this translates into higher expected winter fuel costs, greater uncertainty, and less insulation from events occurring thousands of miles away.

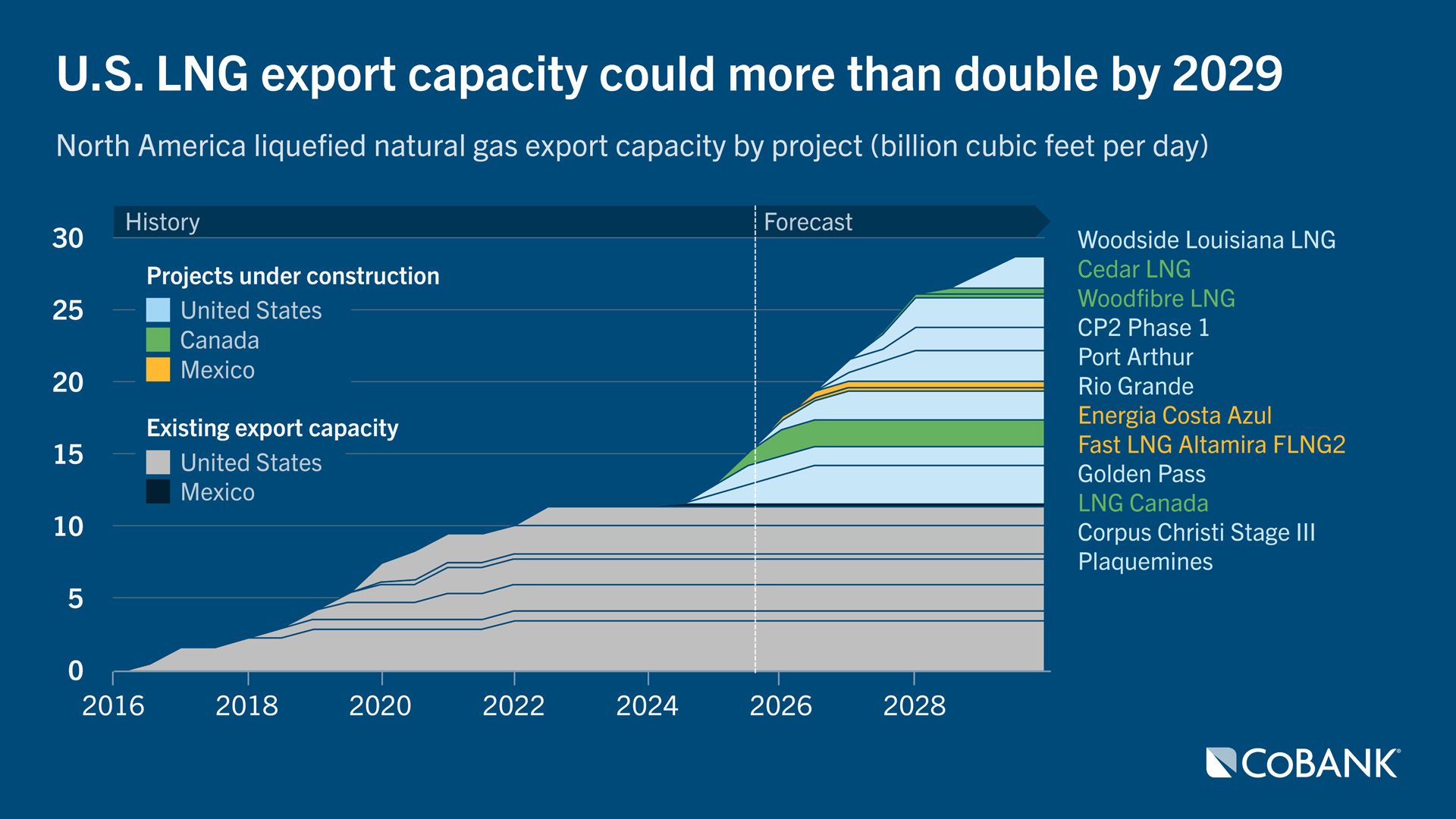

Looking ahead, the global demand for U.S. gas is set to intensify. LNG export capacity under construction or firmly planned could more than double by the end of the decade. Any increase in LNG export capacity in turn increases new demand for U.S. gas that does not disappear when prices soften. This expansion makes demand for LNG more permanent, constant and structural, reinforcing higher price floors and deeper linkage to global markets. It also increases regional basis risk, particularly near the U.S. Gulf Coast and major pipeline corridors feeding export terminals.

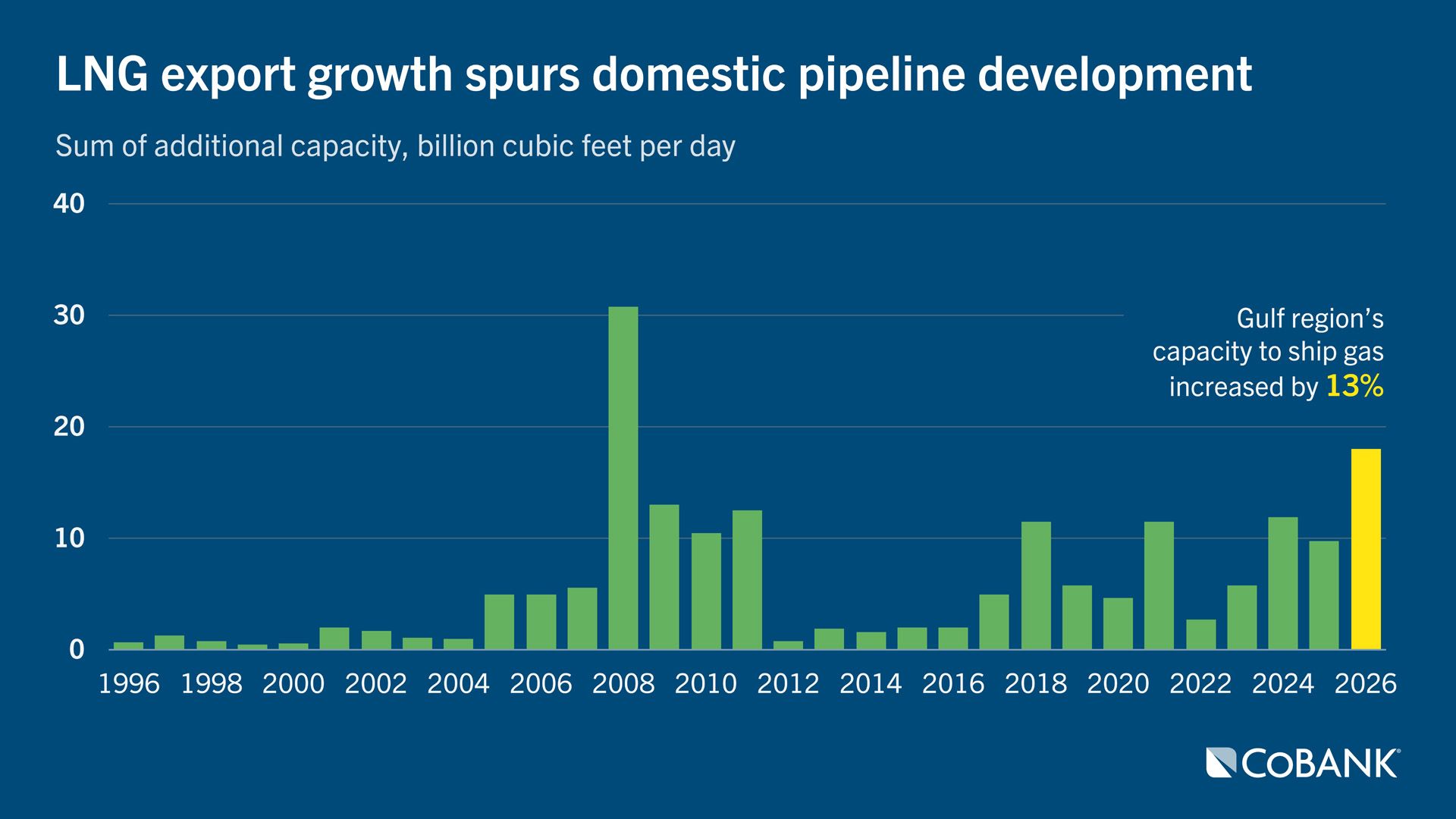

Pipeline development, while extensive, does not necessarily mitigate this risk. Much of the recent buildout is designed to move gas toward LNG facilities rather than broadly rebalancing regional supply. By tying flows more tightly to export demand, pipelines can actually amplify basis volatility. Outages, congestion or LNG maintenance can cause sudden flow reversals or stranded volumes, leading to sharper and more frequent regional price dislocations. For utilities, pipeline expansion no longer guarantees basis relief and may increase delivered cost volatility under stressed conditions.

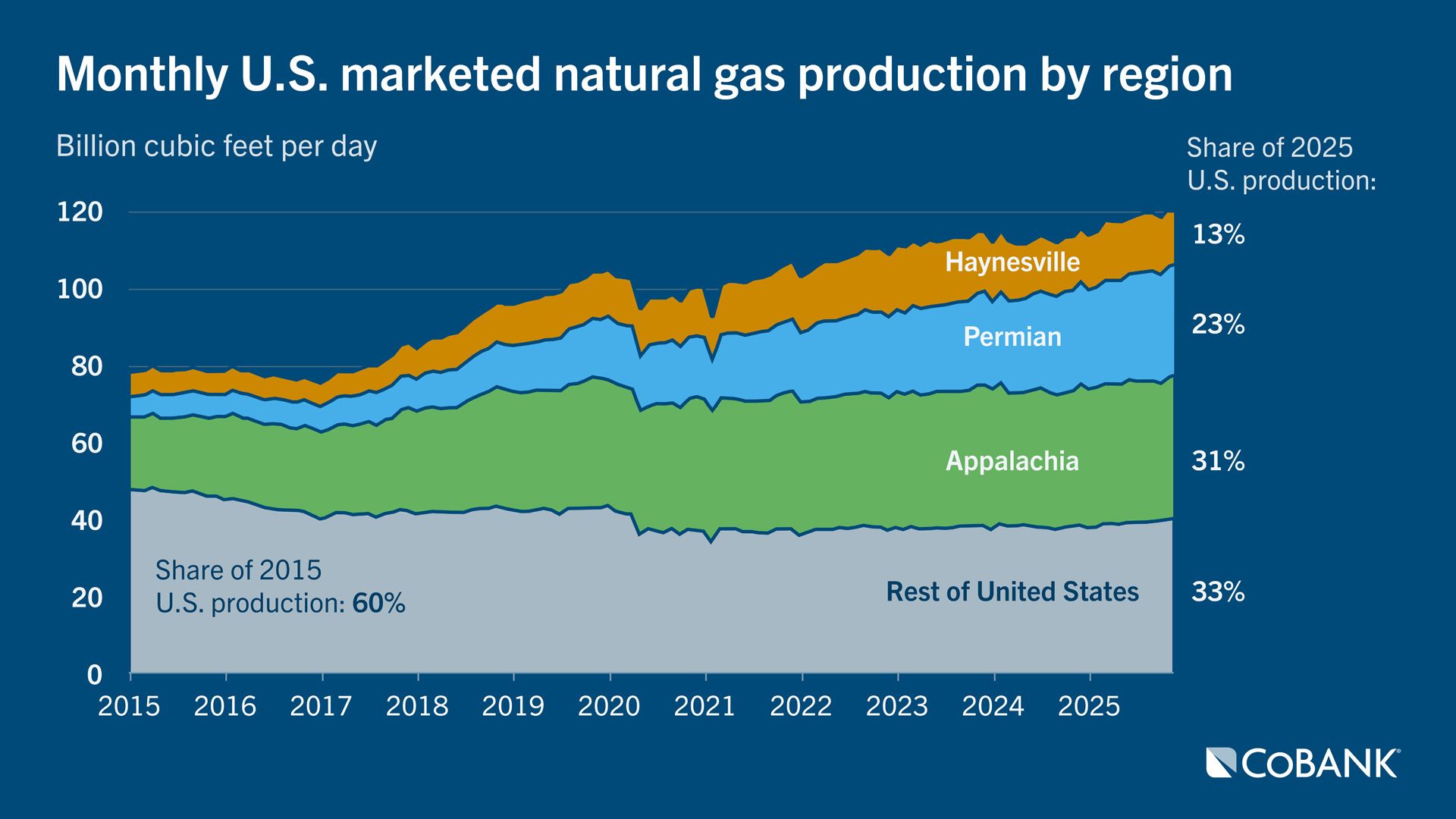

Finally, supply dynamics themselves have become more fragile. A growing share of U.S. gas production — particularly from the Permian Basin — is associated gas linked to oil directed drilling. While higher oil prices can boost gas output, this supply is not responsive to gas price signals. If oil prices fall or drilling slows, associated gas volumes can decline even when gas demand and prices are rising. Combined with significant pipeline constraints in key producing regions, this oil linked supply adds volatility rather than resilience to the market.

In sum, U.S. natural gas has transitioned into a structurally tighter, globally connected system. LNG exports lift the price floor, geopolitical disruptions drive winter and basis volatility, export oriented infrastructure reshapes regional pricing, and oil linked supply introduces new fragilities. For utilities and large gas consumers, the primary risk is not only physical shortages but higher, stickier prices and increased exposure to global events. Long term planning, hedging strategies, and rate design must adapt to this new reality — one in which U.S. natural gas is no longer insulated, predictable, or cheap by default.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.