Food and beverage companies sharpen M&A efforts

Billy Roberts

As consumer packaged goods' prices increased and sales volume has dropped in recent years, mergers and acquisitions within the food and beverage space have ironically followed suit.

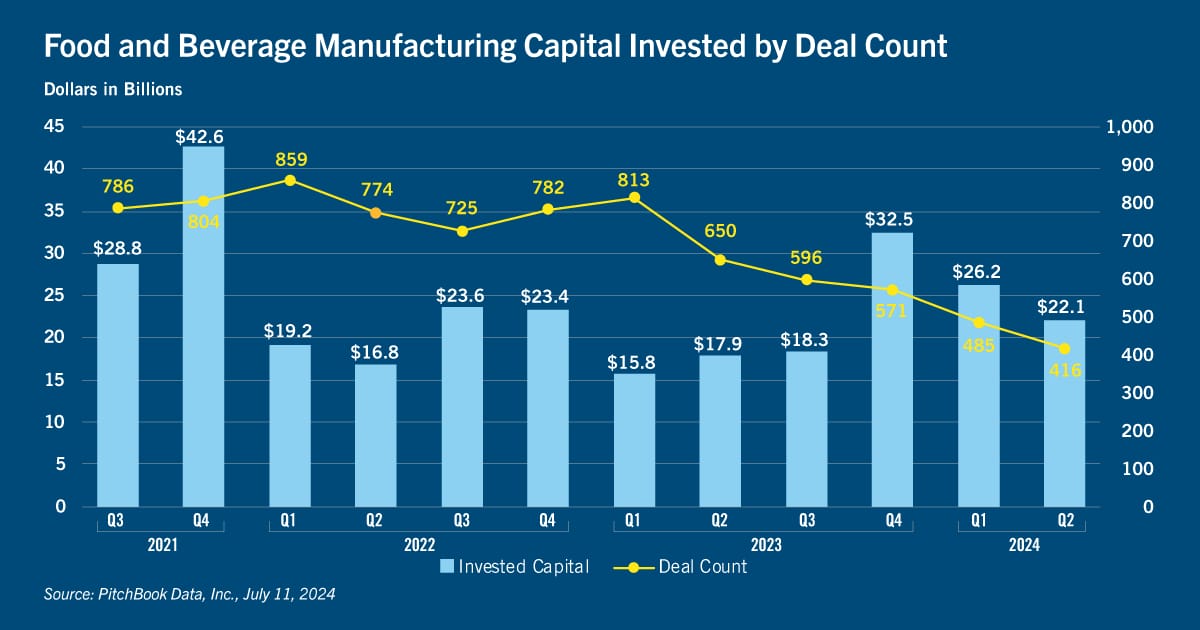

Between the third quarter of 2021 and second quarter of 2023, the total quarterly number of food and beverage M&A deals never slipped below 650, per Pitchbook, with an average per-deal capital investment of $30.4 million. In 2024, the per-deal average increased to $53.6 million per quarter and dropped below 500 – 38.7% shy of the 2021-23 average. However, activity appears to be picking up with expected rate cuts poised to lower the cost of capital to finance acquisitions. In addition, executives from Mondelēz International, General Mills and other CPG firms show openness to M&A activity in their recent earnings calls.

Activity poised to pick up

Several executives attending February's Consumer Analyst Group of New York conference explained they are poised to strike if the right deal presents itself. We have a pipeline. That pipeline is active, Dirk Van de Put, CEO of Mondelēz, told attendees. There are good discussions going on. The Ritz and Oreo manufacturer looks at 35-40 possibilities a year, according to Van de Put. Similarly, General Mills has been looking “at a lot of acquisitions” in recent years but asking prices have been more than his company was willing to pay, according to CEO Jeff Harmening.

Manufacturers are increasingly aligning their SKUs (stock keeping units) around the 80/20 principle (80% of revenues tend to come from one-fifth of their brands) and devoting attention to that more profitable 20%. As a result, they are streamlining portfolios by offloading products or brands that either do not align strategically or increase supply chain complexity. These acquisitions not only reduce some of the pressures on brands’ R&D departments to innovate but these generally smaller-sized deals are also more financially palatable. In fact, several recent acquisitions have been of a smaller variety.

One example is Hershey’s 2023 purchase of two popcorn operations from a co-manufacturer to increase production capacity and flexibility for its SkinnyPop brand. Cal-Maine Foods similarly acquired egg supplier ISE America for $110 million in June, and other acquisitions are likely in the offing. At the Barclays Global Consumer Staples Conference in early September, Flowers Foods noted interest in growing share and is bullish on the M&A market, though any such move would be nothing transformational … focused on expanding our branded portfolio, and there are a few core acquisitions that would help.

Strategic focus underpins recent M&A

This is not to say that CPG M&A hasn’t seen its share of high price tags, but recent transactions deepen companies’ presence in specific areas:

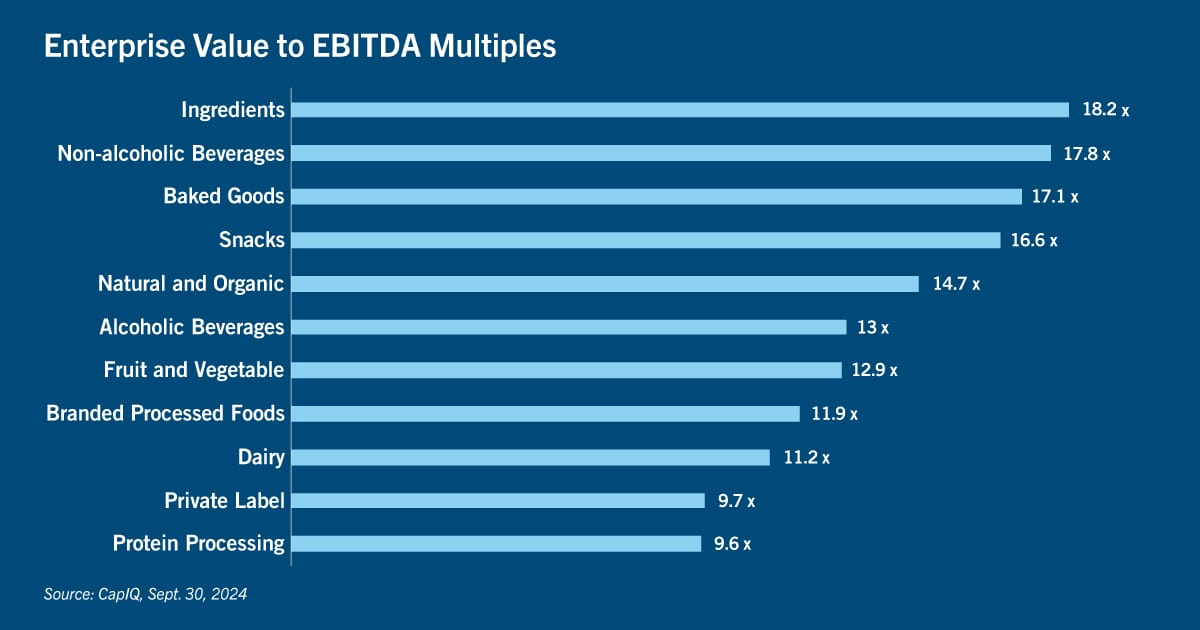

- In 2023, J.M. Smucker bought Hostess Brands for roughly $6 billion, a value roughly 17.2 times the latter’s adjusted EBITDA (earnings before interest, taxes, depreciation and amortization) multiple, per estimates of 2023 results. This purchase expanded Smucker’s presence in indulgent categories and in the convenience store channel.

- Ferrera captured a greater share of confectionery with its purchase of Jelly Belly for an undisclosed amount in late 2023.

- Recognizing its future was not in the dairy case, General Mills recently exited yogurt by selling brands including Yoplait, Go-Gurt, Oui and others to Lactalis for $2.1 billion. This move allowed GM to focus on its brands that have better margins and longer-term growth potential more in line with others in its portfolio.

- Early in 2024, Prego pasta sauce, owner of Campbell Soup, spent $2.7 billion for Sovos Brands (an adjusted multiple of 14.6 times EBITDA), primarily for the Rao’s premium sauce brand that has annual sales approaching $1 billion alone. This purchase has prompted Campbell Soup to adjust its name to eliminate “soup” as a reflection of its focus on brands not only in meals, but also beverages and snacking.

Despite those prominent purchases, M&A activity in the CPG space has slowed in 2024 but with considerable strategic focus. Mars Inc. is expected to pay $36 billion for Kellanova and its Pringles, Pop-Tarts, Cheez-It and Eggo brands, a value 16.4 times the latter’s adjusted EBITDA multiple (as of June 29, 2024). The impetus behind Mars’ purchase is clearly twofold: reach a global audience and expand its snack presence. Mars is far from alone in that snack-oriented M&A aim:

- Cooper Street Snacks purchased Harvest Valley Bakery in September 2024, which is expected to “play a crucial role in supporting the company’s expanding product lines.”

- After purchasing ParmCrisps and the crispy cookie brand Thinsters for $259 million in late 2021, Hain Celestial sold the latter to J&J Snack Foods Corp. in April of this year and the former to better-for-you snack company Our Home in August.

- Our Home has made several other snack acquisitions, paying $182.5 million for R.W. Garcia and Good Health from Utz Brands in early 2024, while also buying Pop Secret popcorn over the summer. These brands join Food Should Taste Good, Popchips, Real Food from the Ground Up, and You Need This, in what the company describes as a better-for-you snacking platform.

Conclusion

With consumers focused on better-for-you snacking, M&A opportunities in those spaces will likely increase, especially as certain segments appear overcrowded. Specifically, categories such as plant-based meat alternatives have a wealth of smaller brands, and with limited category growth of late, consolidation is likely. Elsewhere, major companies have opportunities to expand with strategic acquisitions of smaller players or for smaller companies to build share through merging. In alcoholic beverages, the top 10 beer and lager companies comprise approximately 65% of the market. PepsiCo controls 88% of dip sales, per The Guardian; 93% of the carbonated soft drink space is shared among three companies, the same number who comprise 73% of breakfast cereals, 79% of pasta and 58% of fresh bread. Yet, innovation and growth are seen more at the smaller end of the spectrum. This gives those acquirers the chance to not only align with rising consumer trends but also to focus on growth strategies where their current portfolios are already well-positioned.

References

Russell Redman. “Flowers Foods bullish on M&A market,” Baking Business, Sept. 12, 2024, https://www.bakingbusiness.com/articles/62292-flowers-foods-bullish-on-m-and-a-market

Helana Robbins Huddleston. “Manufacturing M&A Quarterly Report: Q2 2024,” The Food Institute, Aug. 5, 2024.https://foodinstitute.com/focus/food-beverage-manufacturing-ma-quarterly-report-q2-2024/

Surbhi Jain. “Food Sector M&A Is Heating Up,” Benzinga, Aug. 26, 2024. https://www.benzinga.com/trading-ideas/long-ideas/24/08/40562970/food-sector-m-a-is-heating-up-gabelli-fund-manager-says-watch-for-bellring-brands-campbe

Nina Lakhani, et al. “The true extent of America’s food monopolies,” The Guardian, July 14, 2021. https://www.theguardian.com/environment/ng-interactive/2021/jul/14/food-monopoly-meals-profits-data-investigation

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.