Coffee prices jump on flat production, global demand buzz

Billy Roberts

Key points

- Prices of U.S. imported coffee shot up 65% between 2021-23 and have remained volatile well into 2024. U.S. sales have been slipping, with volume sales of ground coffee down 15.7% since 2021.

- Challenging conditions in key growing markets Colombia, Brazil and Vietnam are contributing to the price increases and show few signs of improving.

- Overall global coffee demand is growing, driven strongly by increasing consumption rates in China. In 2023, the number of coffee shops in China grew 58% to 50,000, overtaking the U.S. as the world leader in branded coffee shops.

- The per-unit prices of coffee away from home have surged in the past year, which may lead consumers to reconsider their coffee outings and turn to inclusions and flavorings at home.

Introduction

Since January 2021, U.S. coffee importers – which supply 99.6% of the coffee consumed in the U.S. – have faced escalating costs for the commodity. Import prices jumped 65% between 2021-23, making a serious impact on consumer prices. Per-unit U.S. prices of ground coffee in the past year jumped 20% as of April 7 while sales fell 1.2% in dollars and 3.2% in volume, according to Circana. The longer-term U.S. trends for ground coffee sales volumes are even more pronounced, down 10.1% since 2022 and 15.7% since 2021.

While the COVID lockdowns starting in 2020 forced consumers to shift where they enjoyed their coffee (out of cafes/coffee shops and into their homes), the overall amount of coffee Americans consumed remained steady during the pandemic. And existing stockpiles of coffee reserves offset the price impact of lower imports. However, that changed in September 2021, as reserves dropped, worldwide demand for coffee accelerated, and prices spiked. The YoY price increases have slowed, but they have yet to close the considerable double-digit percentage increases seen from 2021 and into 2022.

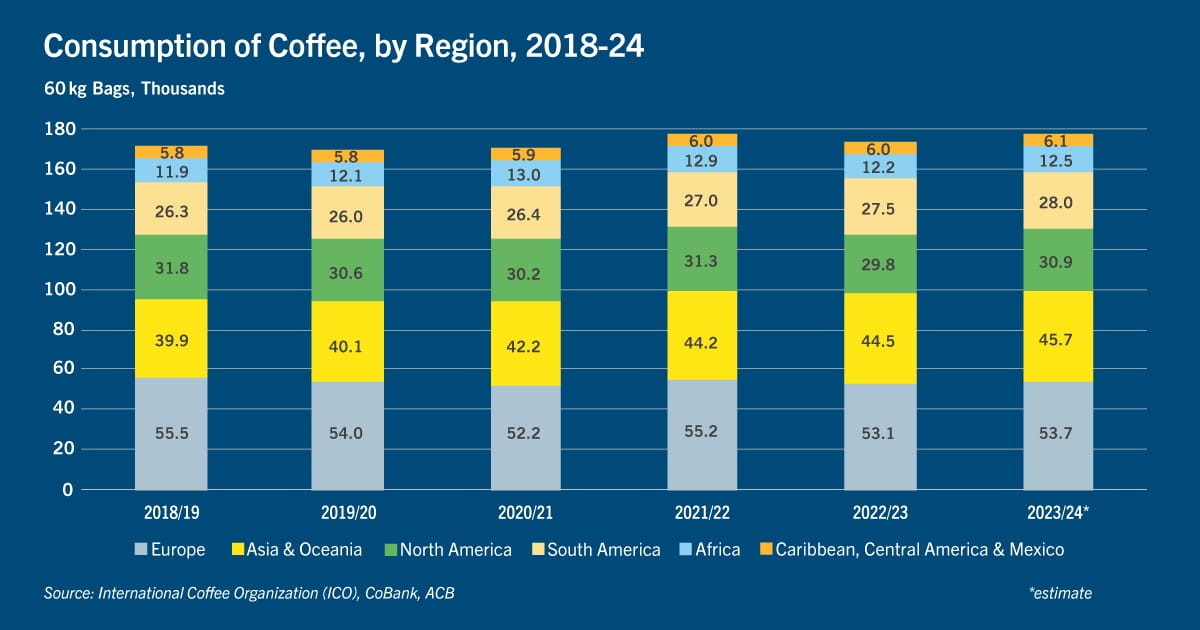

Worldwide coffee demand grows

Even as North American and European coffee consumption has flattened, global coffee consumption has steadily climbed – up 3.4% since 2018. In fact, servings (units) of coffee away-from-home grew 5% YoY globally as of May 1, 2024, outpacing both tea (4%) and carbonated soft drinks (3%). Consumption in Asian countries has jumped 14.5% since 2018, as coffee has become a much more common beverage choice.

China is playing the lead role in driving the world’s coffee demand growth. Servings in China were up 15% YoY as of May 1, 2024, compared with 3% in the U.S., according to Circana. The number of coffee shops in China grew 58% to 50,000 in 2023 alone, overtaking the U.S. as the world leader in branded coffee shops, according to The World Coffee Portal. Tea may remain foundational to Chinese culture, but younger, middle-class consumers are turning to coffee’s caffeine kick.

In the U.S., consumers are still gravitating to coffee drinks, as the National Coffee Association reports the number of Americans drinking coffee daily has grown by 37% since 2004. But the story seems to be in the changing contents of Americans’ coffee cups. The association’s spring 2024 National Coffee Data Trends report found more than half of Americans had a specialty coffee in the past week (57%), a 7.5% increase from a year ago, led by growth in espresso-based beverages (10%). Just under a third (32%) of past-week coffee drinkers had flavored coffee, with vanilla the most popular, followed by mocha, hazelnut and caramel.

Production headaches jolt coffee prices

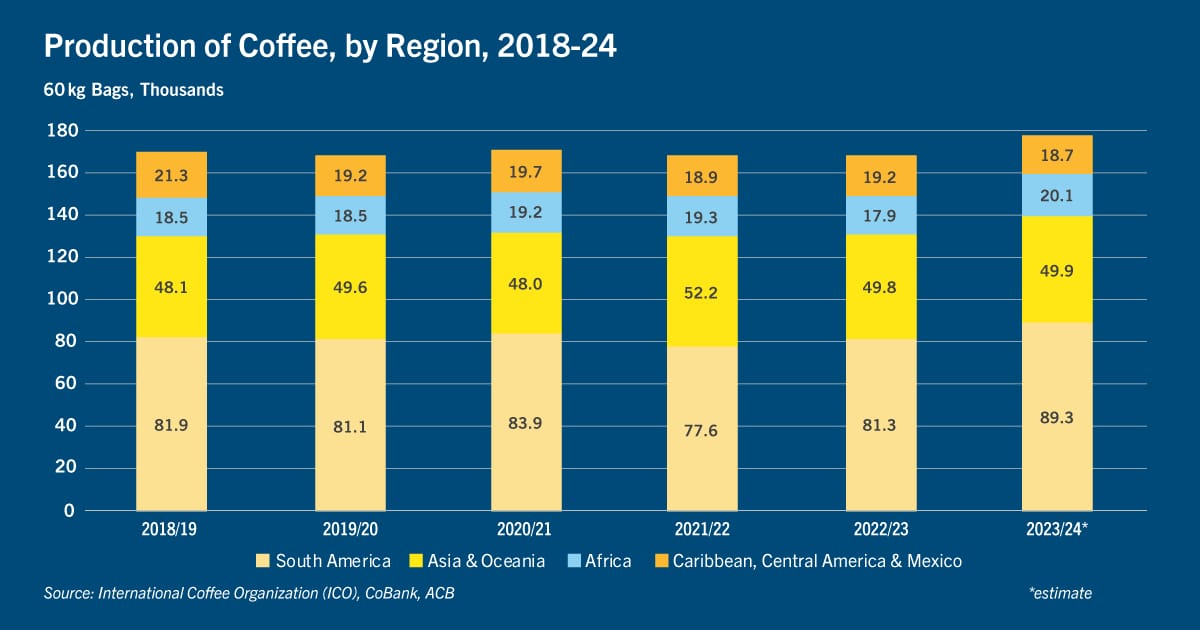

Along with growing coffee demand around the world, larger coffee exporters to the U.S. are grappling with production challenges. Droughts, frost and fires in Brazil have damaged as much as one-fifth of arabica coffee producers’ growing areas, and frost and below-average rainfall continue to hamper progress. Colombia has yet to fully recover its pre-COVID share of U.S. exports; the U.S. saw a 16% decrease in Colombian coffee supplies from 2019-21, with a slight improvement in 2022. In the meantime, Colombian coffee yields continue to trend lower, likely the result of growers opting to limit fertilizer as its price spiked. Vietnam, the third-leading coffee supplier to the U.S., has likewise suffered COVID-related disruptions, with stringent travel restrictions in the country leading to a notable workforce decline. More recently, Vietnam’s coffee growers have also seen severe weather, and the prolonged heatwave in March could negatively impact next year's crop currently in flower. Considering Vietnam grows the bulk of the world's robusta beans, used in instant coffee and espresso, the prolonged damage to the country's crop is likely to push up both futures prices and ultimately, consumer prices.

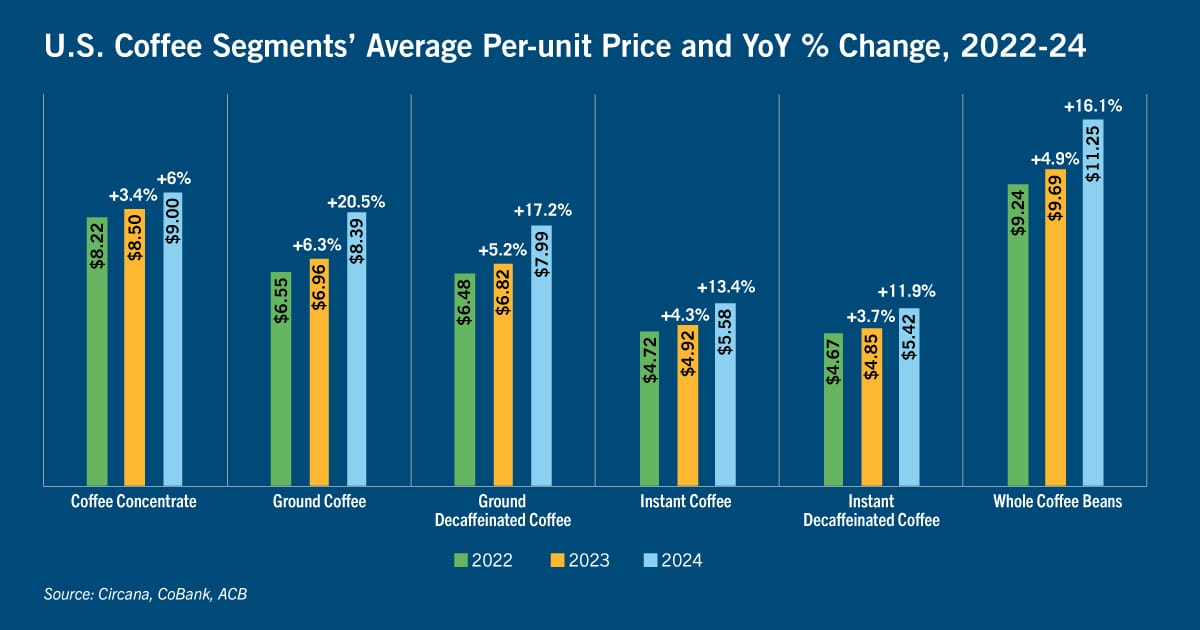

The supply shortages and increased consumption globally has led to unprecedented volatility in coffee prices. U.S. Bureau of Labor Statistics data find prices for U.S. imports of coffee fell 2.6% from May 2022 to May 2023. Yet, even with the drop, U.S. prices remained substantially ahead of their 2021 levels: 57% higher in May 2023 than in May 2021. High U.S. import coffee prices have persisted and are only slightly behind the record-high price seen in 2022. Global crop concerns have pushed up prices of both arabica and robusta (the two major types of coffee Americans consume), and the resulting rise in coffee prices is now being felt by U.S. consumers. The largest coffee segment by far, ground coffee, currently averages $8.39 per pound, 20.5% more than in April 2023 ($6.55). Ground decaffeinated is 17.2% more per unit; in fact, the only coffee segment dodging major price hikes is coffee concentrate.

Fortunately for world coffee markets, the International Coffee Organization predicts 2024 coffee production (178,000 60kg bags) will outpace consumption (176,900 60kg bags) for the first time since 2020-21 as the conditions facing the world's major exporters of coffee appear temporary, if extraordinary. Therefore, coffee production levels should increase, as countries boost their yields and resolve labor concerns, even as interest in and consumption of coffee continues to percolate.

Conclusion

U.S. consumers are likely to continue seeing higher coffee prices until production issues are resolved and global demand climbs. These price hikes may well force consumers to rethink their choice of coffee, likely resulting in a further shift to more at-home coffee occasions rather than from typically pricier coffee shop offerings. At the same time, this consumer response points to opportunities for retail offerings of flavorings such as hazelnut and caramel that could boost premium at-home coffee creations.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.