C-stores evolve from gas-n-grub to true food destinations

Billy Roberts

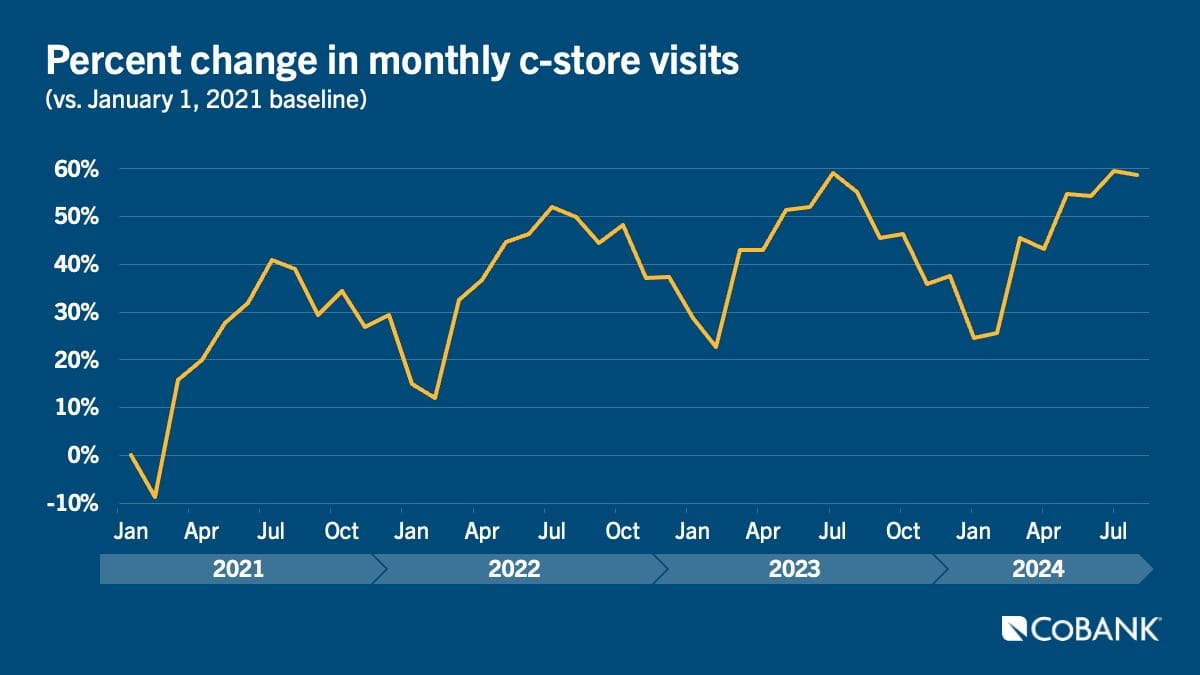

After pay-at-the-gas-pump technology took off in the 1980s, convenience stores faced a challenge: how to draw consumers inside, where more than half simply stopped going, per National Association of Convenience Stores. Fast forward to today, and foot traffic into convenience stores, known as c-stores, has grown 58.6% since January 2021. And since February 2024, overall year-over-year visits to c-stores have risen every month, according to Placer.ai.

What’s pulling customers inside? Food. C-store growth in foodservice options has outpaced that of quick-service restaurant competitors, a trend expected to continue. Technomic projects 2025 growth for all foodservice at 1.9% but 2.3% among retailers including grocery stores that offer foodservice. Datassential foresees a similar breakdown, though slightly lower: 1.5% for c-store foodservice versus 1% overall for foodservice.

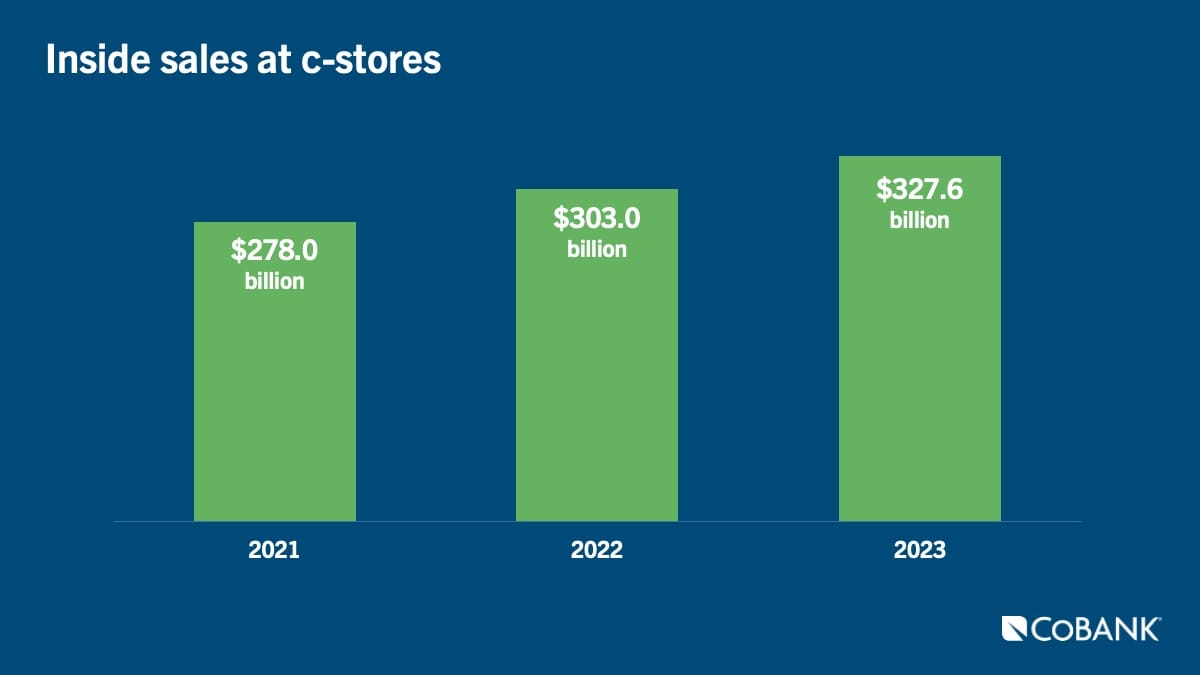

As c-stores registered record sales in 2023, per the NACS, more than a third of the $859.8 billion came from in-store sales ($327.6 billion). The average basket size increased 3.7%, reaching $7.80. This increase reflects the continued, steady growth in in-store sales led by prepared food sales, which grew 12.2%. C-store in-store sales grew 8% YoY in both 2022 and 2023 according to Circana, well ahead of overall inflation numbers for both food at and away from home. While sales appeared to soften in 2024, a Convenience Store News survey found two-thirds of c-store retailers predict total sales per store will grow in 2025.

Loyalty programs, private labels keep ‘em coming back

Another driver behind c-stores’ success is customer loyalty programs, as a number of c-stores have developed loyal followings on a near-nationwide scale. In August 2024, year-over-year visits were up 11.7% for Buc-cee’s, 7.6% at Sheetz, and 3.2% at Wawa, according to Placer.ai. Between January and August 2024, YoY visits to Wawa were mostly elevated, Placer.ai noted. Successful recent stretches like these have helped inspire those brands to expand into new locales as Wawa is venturing into heavily populated Southern states like Florida. Its store count has grown significantly over the past few years, with the state’s 287 Wawas now second only to New Jersey’s 298 Wawa locations.

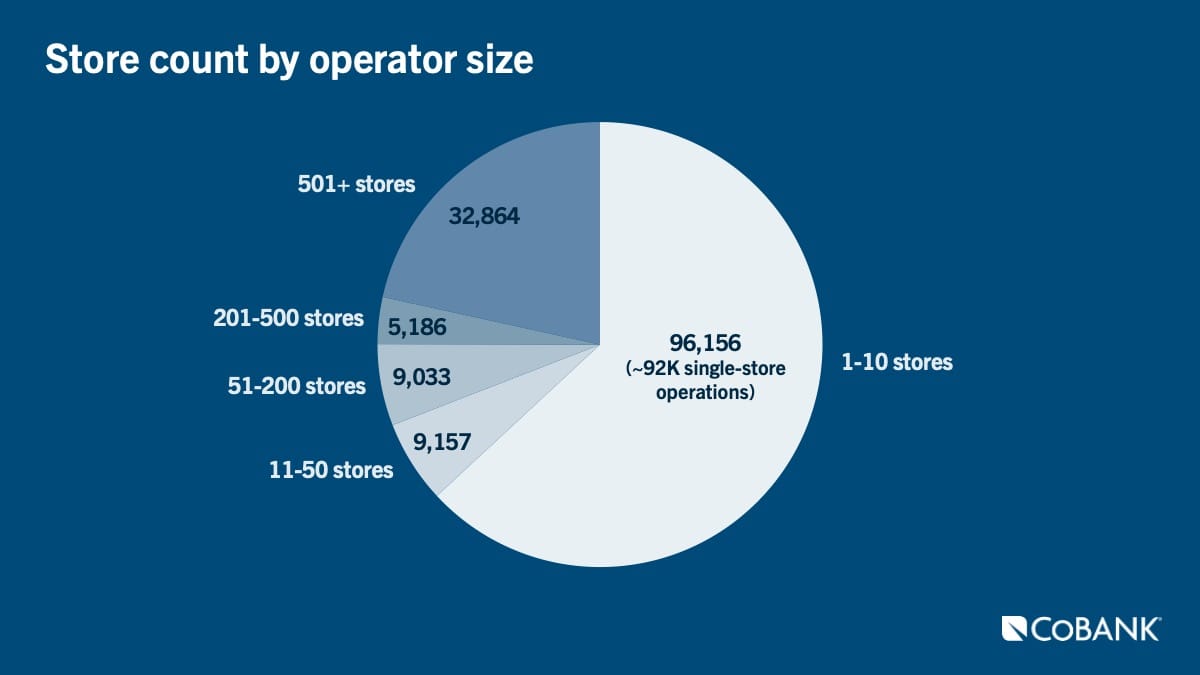

Nevertheless, regionality defines much of the c-store industry. And with so many small entities, the result is a longer-term rapport with their customers and their community, in many cases serving as a de facto grocery solution for food deserts. At the same time, operators large and small are seeking to stand out with signature items, whether pizza at Casey’s, sandwiches from Wawa, Road Ranger’s Omaha Protein Popcorn (a somewhat-indulgent snack but low in sugar and boasting protein) or single-unit Curby’s Express Market, whose tea offerings account for $800,000 in annual sales with 80% margins, per COO Richard Cashion.

A key differentiator from other retailers for c-stores is variety, as even that single-unit Curby’s not only sells up to 500 pizza slices a day but has a novel pizza every week. And with a typically wider range and variety of beverages, for example, c-stores offer a greater degree of choice compared with quick-service restaurants and other foodservice options.

That range of offerings is leading to strong loyalty to c-stores. The 2024 Loyalty Trend Report from Paytronix finds at least 80% of c-stores’ loyalty program members in the top half of loyalty transaction visits per store every month. That rose to 85% for retailers in the 90th percentile and above. For comparison, similarly rated QSRs saw 62% of their loyalty members returning monthly, and full-service restaurants in that range retained 58% of members. This enthusiasm for loyalty programs will be a tool that c-stores look to sharpen as they look to claim more traffic from restaurants, which have seen weak results of late.

Packaged foods and beverages are far from afterthoughts, though. Capitalizing on consumer interest in cost-saving via private label options, several chains have such programs either in place or in development. However, for these retailers, much like grocery chains and mass merchandisers the likes of Walmart and Target, the goal is not simply value but building customer loyalty and repeat visits. Love’s is among those whose private labels are focused on unique products that differentiate it from competitors, in segments such as energy drinks, nuts and seeds, granola bars and confectionery.

7-Eleven is accelerating its private label growth, introducing twice as many items in 2024 compared to 2023. The c-store giant typically garners margins of greater than 50% on private label goods, compared with an average 32% margin on national brand offerings. This is not to say that national brands have no place in the c-store, but with such a vast number of operators, distribution can be a challenge.

Several major food brands have entered the c-store channel through mergers and acquisitions. J.M. Smucker cites c-store distribution as an important reason behind its early 2024 acquisition of Hostess Brands. Similarly, Hormel Foods dramatically expanded its c-store penetration with its 2021 purchase of Planters and Corn Nuts brands, with Hormel utilizing those newfound distribution relationships to bring more of its products to c-stores, including pizza toppings and bacon.

C-store kitchens are seeking quick and easily prepared products. In the process, Hormel is among the suppliers that has found c-stores to be something of a testing ground for new flavors and product concepts, including novel experiments with varieties of Planters Flavored Cashews and Skippy P.B. Bites, with extensions exclusively for c-stores under the Corn Nuts brand. In the case of Hormel’s Bacon 1, the key distinction isn’t necessarily flavor but ease for the operator. The fully cooked option is quickly heated and thereby added a host of options to c-store menus, possibilities that had been relatively off-limits due to labor difficulties and the challenges of raw protein preparation.

Foodservice is the future

Seeking to gain share of the $1,200 the average American spends annually on quick service restaurants, per Supermarket News, travel centers and convenience stores have long partnered with QSRs to bring established restaurant names like Arby’s, McDonalds and Subway onto their sites. However, several c-store retailers have added more unique eateries. Gas N Wash plans for two co-located Mickey’s Greek-style restaurants, and Love’s Travel Stops & Country Stores has expanded its agreement with Naf Naf Middle Eastern Grill to three more sites, setting a target of 11 locations for the partnership.

Foodservice for the channel represented 26.9% of in-store sales, a 1.3% increase over the prior year, with strong consumer interest in prepared food, commissary, and hot, cold and frozen dispensed beverages. That said, there is a risk that c-stores are vying for a decreasing portion of consumer purchases. In the second and third quarters of 2024, Circana reported year-over-year declines in dollar sales for consumer-packaged goods products in the convenience channel, driven by decreases in unit sales and trips per consumer, as well as a decline in fuel volume per buyer. Nevertheless, c-stores overall continue to boost their food offerings – both packaged and prepared – to drive traffic.

Increasingly, c-store chains are viewing QSR and fast food as their chief competition and are tailoring their offerings to match if not exceed that found in QSR and limited-service restaurants (LSR), such as Panera Bread, Firehouse Subs and The Habit Burger Grill. Such innovation is not without significant investment, however.

Sheetz is building a $145 million distribution facility to support growth in multiple states and plans to open more than 60 stores in southeast Michigan, all featuring a restaurant-style experience with made-to-order foods, self-service kiosks and drive-thrus. A similar food focus is in the works for Stinker Stores, as part of its in-house fresh food program begun nearly two years ago across most of its 100-plus c-stores. Stinker’s Pete’s Eats has performed so well that the chain is remodeling and building new stores to emulate QSR.

Love’s is investing between $2 million and $7 million to “refresh” a third of its more than 600 sites, all part of a $1 billion store-renovation project the chain is rolling out across the country. Pilot’s New Horizons Initiative, in the works since 2022, aims to remodel all 400 of the chain’s c-stores within three years, with roughly 150 completed as of mid-2024. And while chains like Buc-ee’s and Wawa garner headlines for opening the world’s largest convenience store (a title that changes several times a year), other c-stores have expanded vertically. QuikTrip has a two-story store in Ft. Worth, Texas; Rutter’s added a second floor to its York, Pennsylvania, store; and RaceTrac is opening a two-story location in Cobb County, Georgia.

Conclusion

Convenience stores have evolved from their gas-fueled beginnings to being food and beverage destinations, with a number of larger chains garnering considerable loyalty nationwide beyond their regional origins. However, many c-stores remain single-unit operations, which may bring with it opportunities for some consolidation but also an element of being part of their respective communities.

Likely, the line between grocery stores, QSRs/LSRs and c-stores will continue to blur, intensifying competition and leading to alliances between one or more. Fast-food and sandwich outlets in both c-stores and grocery are common, and supermarkets will continue to cater to the convenient needs of consumers with small-store concepts that draw distinct inspiration from c-stores’ size and offerings. At the same time, expect c-stores to likewise emulate these competitors with a greater variety of freshly prepared items and with more attention to private label products and signature menu items.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.