Gasoline demand has peaked, and that’s a problem for diesel production

Teri Viswanath

AAA projects a whopping 37.1 million road-tripping Americans will journey 50 miles or more from their homes this Memorial Day weekend, the third most since 2000, when AAA started tracking holiday travel. However, despite upbeat signs like this, the nation’s peak gasoline demand is squarely in the rear-view mirror.

While COVID-19 might have permanently altered the nation’s work-commute habits, fuel efficiency and vehicle manufacturing have more to do with the underlying downtrend. Last month, the EPA proposed a vehicle emissions rule that would require up to two-thirds of all new vehicle sales to be zero-emission by 2032. Targeted federal policies and planned obsolesce of gasoline cars will further drive down demand with a “carrot” (Inflation Reduction Act EV incentives) and “stick” (EPA GHG limits for light-duty and medium-duty vehicles). All told, analysts see annual gasoline demand declining from a peak of 9.3 million barrels a day in 2018 to just 7.4 million by 2030.

In the meantime, demand in the harder-to-de-carbonize segments — diesel and jet fuel — will likely increase. The mismatch in transportation trends poses a particular challenge for the country’s 130 refineries and may ultimately impact domestic jet fuel and diesel consumers.

For CoBank and its customers, this is no small matter, as the U.S. agricultural economy runs on diesel. Diesel engines power about 75% of all farm equipment, transport 90% of farm products, and pump about 20% of agriculture’s irrigation water in the United States. Diesel engines power 96% of the large trucks that move agricultural commodities to railheads and warehouses. Diesel powers 100% of the freight locomotives and inland barge and towboat marine vessels that transport bulk harvested crops such as corn and grain to processing facilities.

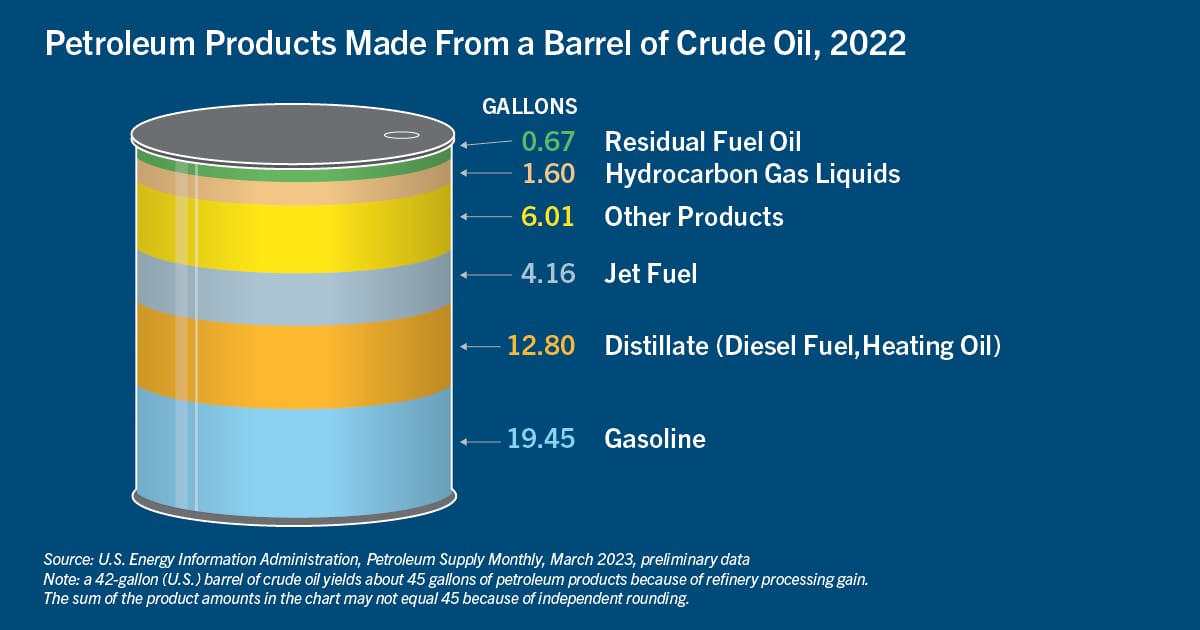

The U.S. is the world’s largest consumer of gasoline, and the nation’s refineries are configured to maximize gasoline production. As such, they have limited ability to change the composition of refined products, which include diesel and jet fuel. According to the EIA’s latest update, a U.S. 42-gallon barrel of crude oil yields about 45 gallons of petroleum products from U.S. refineries, with 43% of the yield concentrated in gasoline production, 28% in distillates (diesel and heating oil), 9% in jet fuel, and 13% in a range of lower-value products. Consequently, lower gasoline demand generally means less need for refining capacity overall, which could create shortages for the rest of the refined products. Alternatively, by continuing to operate at the same utilization rates, discounts for surplus gasoline would need to be made up for by pricing the rest of the refined barrel at a premium.

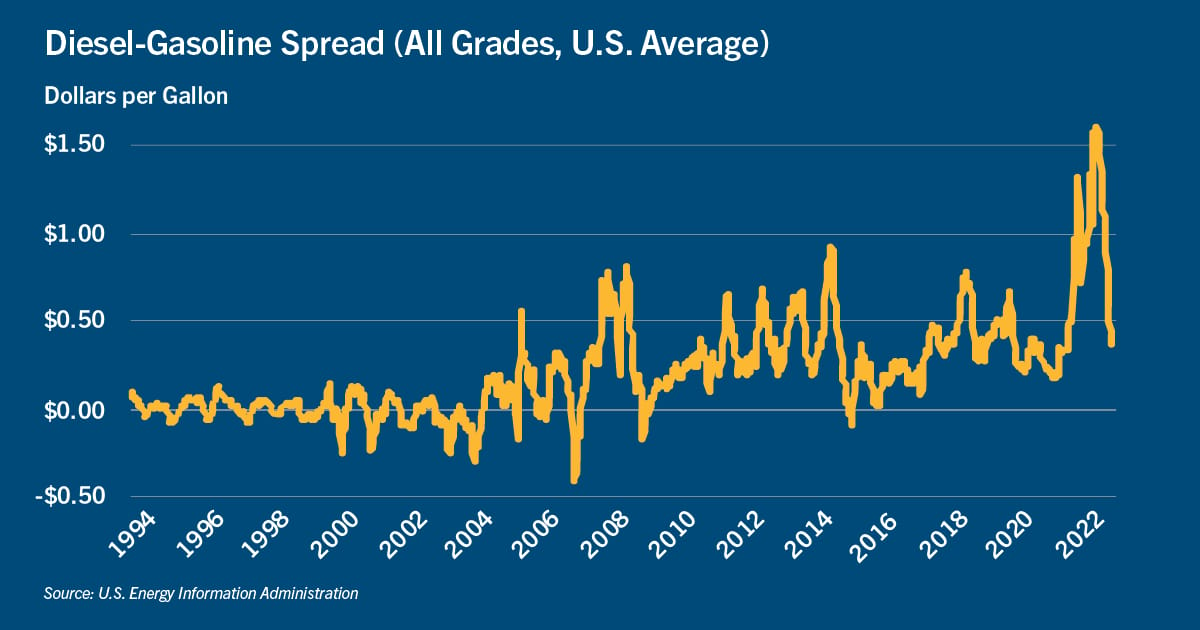

Historically, the gap between diesel and gasoline prices has been relatively small but has recently widened significantly. Leading up to last year’s blowout, diesel prices for the previous five years averaged just 38 cents per gallon more than gasoline. Last year, diesel buyers were paying an average of $1.04 a gallon more for their fuel, disproportionately driving up the cost of practically every product on the shelf and putting a strain on farmers.

As the economy began to slow this year, U.S. inventories of diesel, heating oil and other distillate fuel began to build, re-aligning the transportation pricing spread. Still, given the structural changes on the not-so-distant horizon, the diesel premium could once again begin to build. Indeed, over the long run, the rising price of diesel — a primary economic input and the fuel that moves trucks, trains, barges, tractors and construction equipment — will ultimately be shouldered by all consumers.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.