Russia’s smaller wheat harvest expected to drive market volatility

Tanner Ehmke

Key points

- Russia’s weather-induced production shortfalls and slipping export capacity is expected to awaken the world wheat market to the extreme global tightness that has been building in recent years.

- World wheat prices have been on a roller coaster ride, rallying in recent weeks on crop losses from drought and frost in key wheat-growing regions of Russia then succumbing to harvest pressure in the U.S. and an import ban in Turkey. The risk of extreme volatility in wheat prices remains a post-harvest reality.

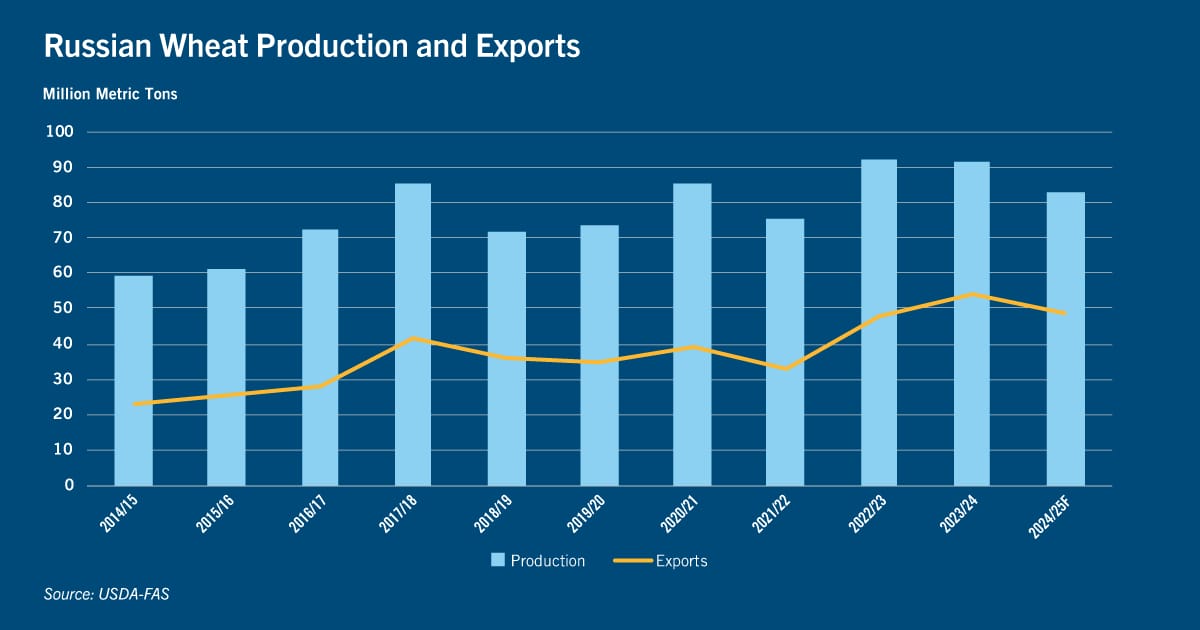

- The crop losses in Russia, the world’s top wheat-exporting country accounting for 25% of all wheat shipments in the 2023/2024 marketing year, come at a time when world stocks-to-use ratios are historically tight.

- The Russian crop must be watched closely in the next month. Once harvest pressure in the Northern Hemisphere subsides and Turkey lifts its import ban, extreme volatility is in the offing for wheat futures, FOB prices, basis, and spreads.

- Sharp price rallies will result in steep margin calls on short positions held by grain merchants. CoBank relationship managers will be necessary resources for emergency lines of credit for rapid run-ups in prices.

Russian wheat outlook

While Russia firmly maintains its hold as the world’s top wheat exporter, Russia’s slippage in production and export capacity is expected to awaken the world wheat market to the extreme global tightness that has been building in recent years.

Russia, the world’s top wheat-exporting country that accounts for a quarter of all world wheat exports, faces a substantial shortfall in production this year from drought in the key southern and central regions and freeze damage in May. A slow seeding pace in Siberia due to wet weather risks further losses in Russian spring wheat production from smaller planted acreage.

USDA-FAS now forecasts the Russian wheat crop to be 9.3% smaller YoY than last year’s harvest at 83.0 MMT (million metric tons). USDA’s estimate remains above private Russian industry estimates such as IKAR at 81.5 MMT, SovEcon at 80.7 MMT, and Rusgrain Union at 79.5 MMT. The Russian government estimates the crop at 86.0 MMT. With a smaller crop, USDA-FAS sees Russian wheat exports falling 11.1% YoY to 48.0 MMT.

Russia’s ability to harvest record crops and quickly export the record surplus onto the world market with the tailwind of an ever-weakening currency has lulled the world wheat market into complacency.

More recently, the historic tightness in world wheat has been masked by the bearishness of several factors: Harvest pressure in the U.S. where wheat production is up 3.5% YoY, ample U.S. corn stocks, and Turkey’s recent ban on imported wheat from June 21 through mid-October to protect Turkey’s farmers from price decreases. Last marketing year, as the world’s second-largest wheat importer behind Egypt and the world’s top flour exporter, Turkey imported 12 MMT of wheat with Russia supplying over two-thirds of Turkey’s imports. With Turkey’s export ban in place, Russian wheat will leak into other foreign markets, pressuring local prices.

Market volatility

In an early sign that Russian supplies are tightening, cash prices for Russian wheat have been quickly climbing with FOB (free on board) prices at Novorossiysk, Russia, up 17% in the last two months. Although Russian wheat exports continue to move at a record or near-record pace, the rise in prices hints the Russian crop may be worse than currently expected.

In another sign of a global shift in wheat market dynamics, Egypt eschewed Russian wheat in its latest two tenders and opted instead for Ukrainian and eastern European origin. Russian wheat offers were well above competing offers in both tenders, which is a rare occurrence. The quick rise in Russian wheat prices raises the question over Russia’s use of export bans or taxes. Historically, Russia has used export restrictions on grain to contain food inflation. In the most notable example, Russia banned wheat exports in 2010 following a poor Russian wheat harvest. This sent global wheat, flour, and bread prices to historic highs. The ban was widely thought to have contributed to the Arab Spring.

This time, Russia’s government has substantially greater control over trade flows with only four merchants authorized to handle exports after Western grain traders exited Russia following its invasion of Ukraine. With greater consolidation of the Russian grain trade, there will be less need for the government to use export bans or taxes to limit trade flows. Restrictions may simply come through reduced offerings from the few firms handling Russia’s wheat shipments.

Russia’s minister of agriculture also recently stressed that Russian exporters will not face difficulties exporting wheat despite Turkey’s import ban, with the underlying implication being that export restrictions by Russia’s government are not on the table. Russia’s ministry of agriculture also recently declared a federal emergency in 10 regions because of frost damage that occurred in May, but no export restrictions were imposed.

Outlook

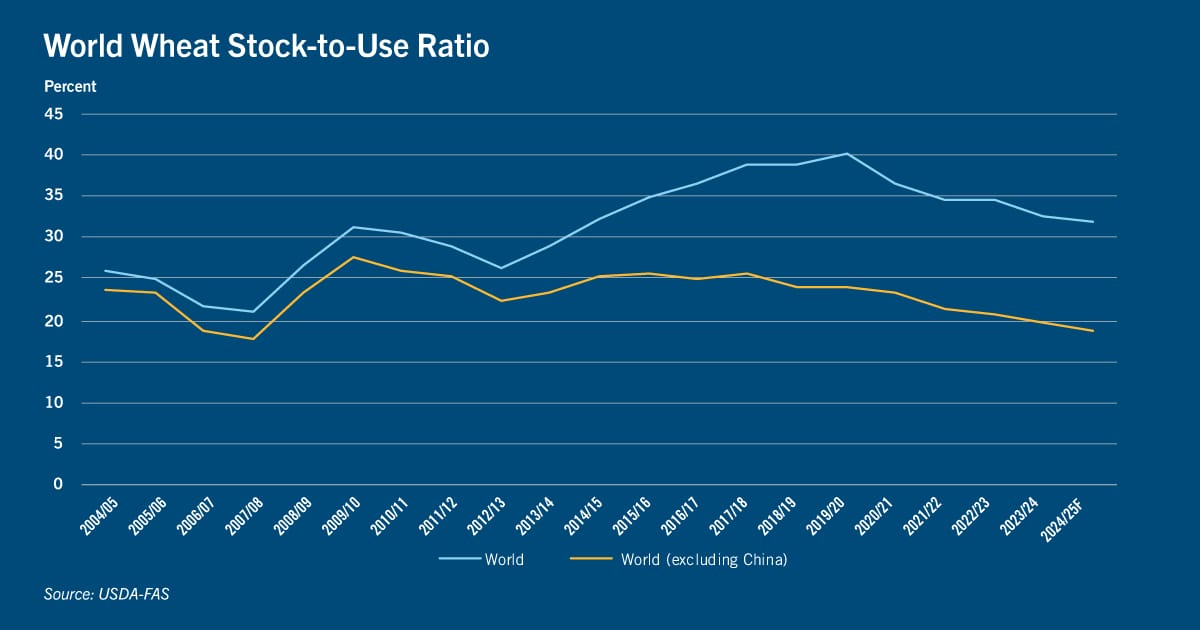

A close eye must be kept on the Russian harvest over the next month for confirmation of the size and quality of the crop. After harvest pressure abates in the Northern Hemisphere and Turkey’s import ban expires, the wheat market is at risk of extreme volatility with Russia’s smaller harvest exposing the tightness in world inventories. The world wheat stocks-to-use ratio outside of China (which holds more than half the world’s wheat inventories, with those stocks being state-owned and non-tradable) has fallen to 18.7% – the lowest level since the 2007/08 marketing year. However, other major exporters like Canada, Argentina and Australia may increase wheat acreage in response to higher prices or experience more benign growing conditions, which would help ease the potentially low stocks-to-use ratio.

The U.S. stands to benefit from a much stronger export program if Russia’s wheat harvest prospects continue to decline, resulting in a tighter U.S. balance sheet. Extreme volatility in wheat futures, cash FOB prices, basis and spreads is expected to unfold in the coming months. In a worst-case-scenario, governments could exacerbate market volatility with restrictions on trade. A larger speculative presence in markets will also increase the level of price volatility compared to the Russian drought in 2010. Sharp rallies will result in steep margin calls on short positions held by grain elevators. CoBank relationship managers will be necessary resources for emergency lines of credit for rapid run-ups in futures prices.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.