Two reasons why lower fertilizer prices won’t shift spring planting decisions

.png?auto=webp&format=pjpg&quality=80)

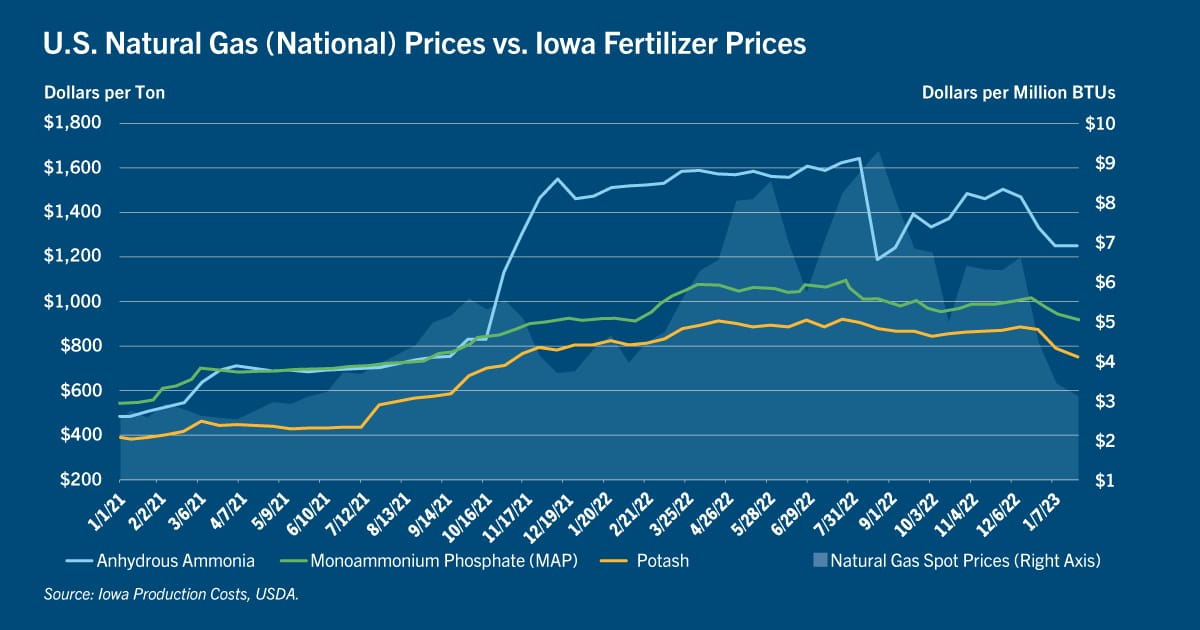

To the surprise of most observers, wholesale fertilizer prices and natural gas prices have been declining since last fall, both globally and in the United States. Although we had expected both prices to rise in late 2022 and early 2023 due to the massive cut in gas supplies Russia imposed on Europe for supporting Ukraine in the Black Seas conflict, the angst proved premature. Instead, Europe built up its natural gas reserves through conservation efforts, used less due to the warmest winter there in a decade, and received record U.S. LNG exports.

Fertilizer production is bound to natural gas — as a feedstock, an energy source, or both depending on nutrient type. Thus the drop in gas prices tends to lead to an across-the-board fall in fertilizer prices, but most notably for nitrogen. From peak-to-trough over the past nine months, U.S. natural gas prices have declined by 67%, compared to price drops of 24% for anhydrous ammonia, 16% for phosphate (MAP) and 18% for potash.

Assuming this recent and rapid drop in natural gas prices holds through spring, we would expect fertilizer prices to continue their downward trajectory in the coming weeks and months. This could change, however, should the Chinese economy reopen and/or the European economy recover, either of which could lead to higher energy prices. And should the Black Seas conflict escalate, a voluntary or involuntary reduction in Russian fertilizer exports could drive up fertilizer prices.

Farmers’ plans are set, but co-ops risk asset impairment

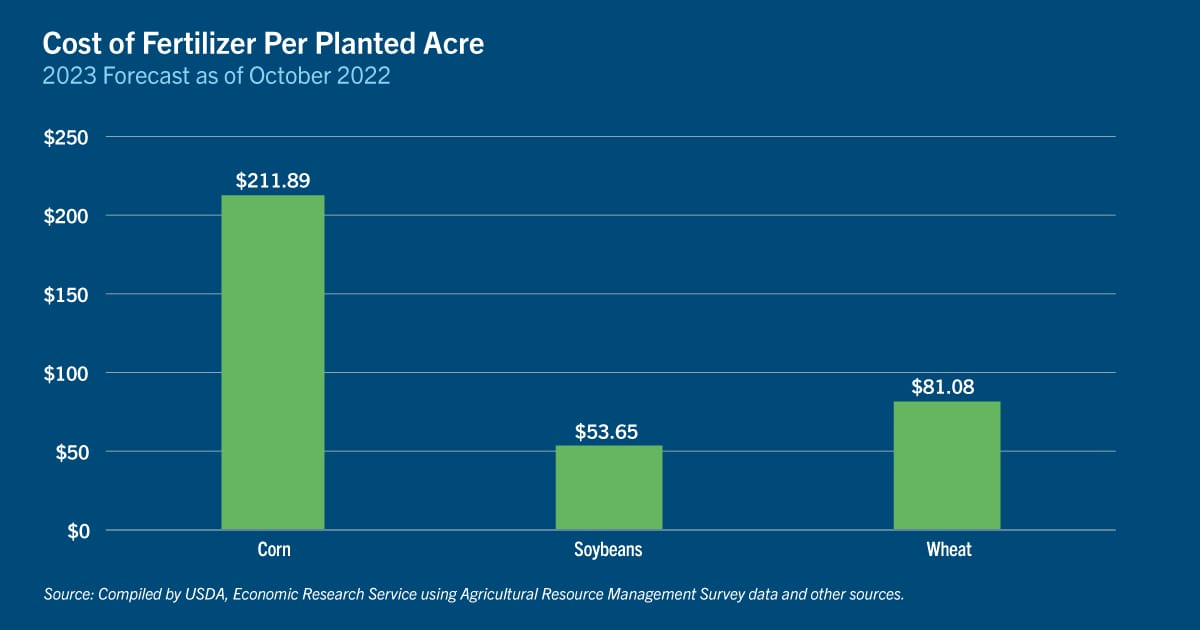

That brings us to spring planting. When fertilizer prices decline by double digit rates ahead of planting season, the next question is whether falling prices of fertilizer — the largest operating cost line item for most crop farmers — might influence their spring planting intentions. The assumption is that lower fertilizer prices ought to drive greater corn acres relative to soybean acres. This is because corn uses more expensive nitrogen fertilizers (such as anhydrous ammonia) than soybeans use. (USDA estimates that the total operating and overhead costs to raise U.S. corn is approximately $870 per acre compared to $591 per acre for U.S. soybeans, largely due to the fertilizer-intensive nature of corn.)

While the argument works in theory, it tends to fail in practice for at least two reasons. According to our farm supply cooperative customers, most farmers have already pre-paid for a sizable portion of their 2023 fertilizer needs based on their crop plans, and thus unlikely to switch acres now. The other factor is that farmers who plan to plant spring corn often apply nitrogen to fields in the fall. Since nitrogen is generally not used in soybean production, farmers will stick with their corn crop decision unless they skipped the fall application.

The bigger concern for fertilizer dealers is the potential risk of asset impairments. For example, if an ag retailer/farm supplier built up fertilizer inventories at peak price levels during 2022 for resale in 2023, the organization could be forced to write down the value if the seller’s wholesale acquisition cost exceeds the retail price at delivery.

While still a risk today, we believe this risk was larger and more pervasive during the 2008/09 fertilizer price spike. Back then, more farmers bought fertilizer on margin and a large number of retailers got caught with inadequate purchase agreements and down payments. When prices fell, those highly leveraged farmers reneged on their fertilizer purchase agreements for spring. The net result was that ag retailers took the hit and ended up writing down the value of their fertilizer inventories.

What co-ops learned from 2008/09 fertilizer price spike

The fertilizer market will inherently always have a price risk element due to lack of formal hedging instruments. However, conversations with CoBank clients suggest that ag retailers have taken steps to avoid painful write-downs this time around. They’ve significantly increased their prepayment programs (i.e., requiring farmers to pre-purchase product), spread out their fertilizer purchases, and strengthened internal risk management processes. And with grain prices remaining high and farms still turning a profit, we believe that ag retailers will be able to better maintain retail prices despite the decline in wholesale prices.

Bottom line, we do not think that fertilizer prices will be a major driver of planting decisions this spring, but stay tuned. We will be paying close attention to USDA’s annual Agriculture Outlook Forum in February and Prospective Plantings report on March 31, as well as private farmer planting intention surveys, temperatures and precipitation levels now through late March, and futures prices for late summer and fall harvest.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.