Five timely trends shaping telecommunications into 2023

Jeff Johnston

Updated December 7, 2022

Rural telecommunications are one of the most dynamic markets in the U.S., fueled by fascinating and durable tailwinds that will push companies through 2023 and beyond.

For example, we are witnessing unprecedented levels of investment to expand broadband access. The data center market is bracing for exponential growth. And big tech companies are pouring billions of dollars into virtual reality applications, which will be mainstream sooner than expected. Meanwhile, private communications companies are taking a star turn as their market valuations continue to outshine those of their publicly traded counterparts.

Here are five notable market-moving developments to watch.

1. Private wireless networks can connect the farm. Previously unserved businesses and organizations in rural America have found an affordable solution in these carrier-grade networks. The business case for farmers, who need high-speed broadband to leverage precision agriculture technologies, is compelling. According to The Ohio State University, farmers are willing to pay between $10 and $30 per acre for broadband. That means a grower with 8,000 acres is willing to pay up to $240,000 for coverage. However, CoBank’s modeling indicates that a 50-member cooperative can a build a private wireless network for around $55,000 per farmer with the same acreage – up to 77% less than they expected.

2. Meteoric rise in the datasphere is coming. The metaverse, autonomous vehicles, migration to the cloud: The demand for data processing and storage will only skyrocket. In 2020, the global datasphere, or the total volume of data created in that year alone, was about 64 zettabytes. Datacenter infrastructure to support the 64 zettabytes in 2020 was estimated to cost $2 trillion dollars. By 2035, self-driving cars alone will spike the datasphere to an estimated eye-popping 10,000–15,000 zetabytes. Suffice it to say, the additional capital required for infrastructure, fiber, and datacenters to support 10,000 zettabytes will be astronomical.

3. Fully immersive AR/VR has a need for speed. Big tech companies have recently announced levels of spending on augmented and virtual reality applications that signal accelerated development and time to market. Meta is spending a minimum of $10 billion a year on AR/VR. Apple and Microsoft haven’t been as explicit about their investments, but rest assured, they’re in the billions. Fully immersive AR/VR applications will require home broadband connection speeds of 200 to 5,000 Mbps. In addition to ultra-fast networks, AR/VR will need data centers located close to where the applications are being used.

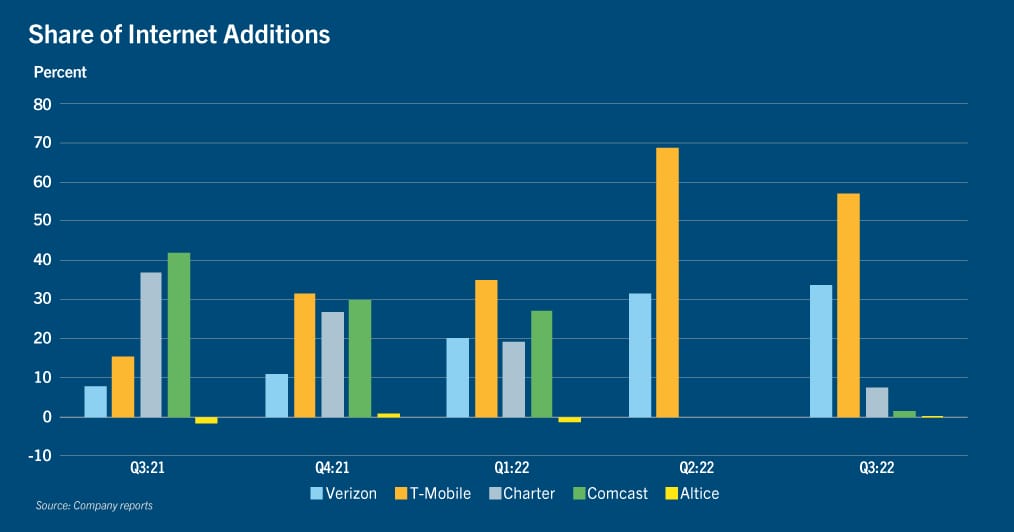

4. Wireless providers are competing for home broadband. National wireless operators are making big gains in the home broadband market with their fixed wireless access offerings as they take market share from incumbent cable companies. In Q2 2022, FWA providers claimed 100% of broadband net subscription additions. (FWA market share is calculated by comparing T-Mobile and Verizon’s FWA additions to Comcast, Charter and Altice fixed-line broadband additions.) That’s quite a jump from Q4 2021 when it was 43%. T-Mobile already covers 30 million homes with FWA and is targeting second- and third-tier markets where they typically have excess network capacity. Verizon plans to cover 30 million homes by 2023 and is focusing primarily on urban markets. Meanwhile, Charter Communications, Comcast, and Altice USA aren’t taking chances and have all launched wireless services via mobile virtual network operator (MVNO) models. They bundle their broadband service with smartphone plans and phones, a strategy that is paying off with subscriber growth.

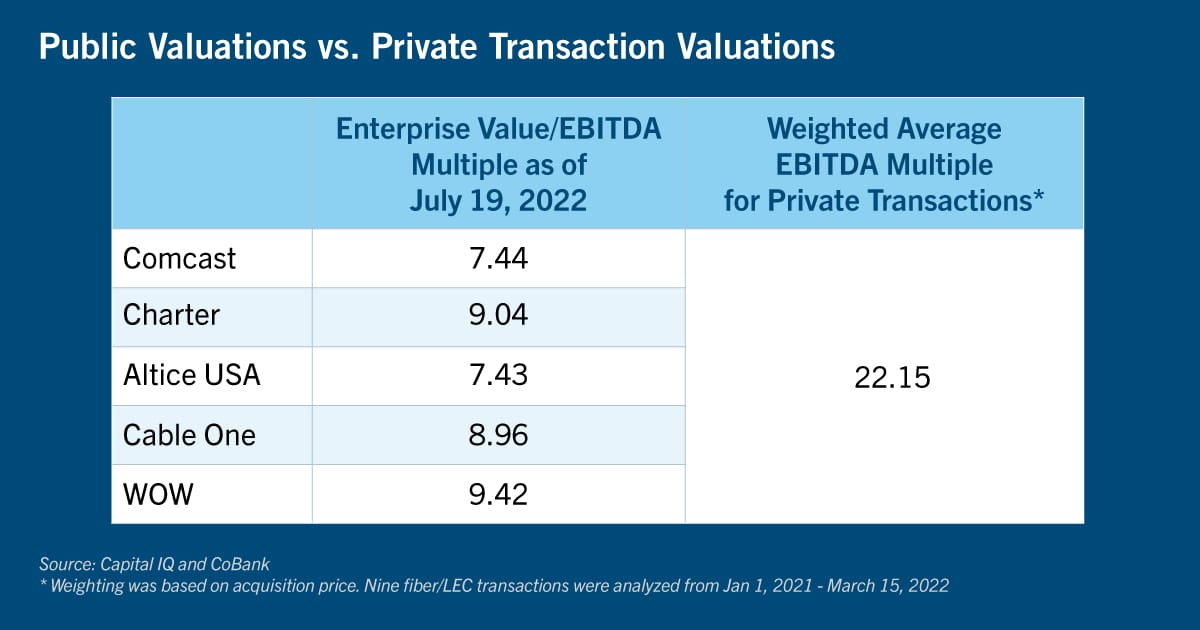

5. Valuations soar for private broadband companies. The valuation gap between private communication companies and public cable companies is the widest we’ve ever seen. Based on recent transactions, valuations for private companies are more than two times higher than the average valuation for the main publicly traded cable companies. Several factors are driving this gap, including strong M&A interest from institutional investors. Electric co-ops that have deployed broadband networks are well-positioned to enjoy similar valuations given their brand equity, strong balance sheets, and similarities to competitive fiber operators. Despite these tailwinds, as we enter 2023 with rising interest rates and recession warnings signs flashing red, it’s reasonable to assume some downward pressure on private valuations.

To sum up these five trends, it comes down to one word: more. More money, more technology, more speed, more competition, more data storage. We are swiftly moving into the digital era.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.