Higher food inflation, slowing economy dampen dairy demand

Rob Fox

Average U.S. mailbox milk prices have dropped more than $6.00/cwt since peaking last May. While milk supply here and in Europe has been edging marginally higher since late 2022, we would argue that the price decline is largely due to broader economic factors that are limiting dairy demand both in the U.S. and abroad.

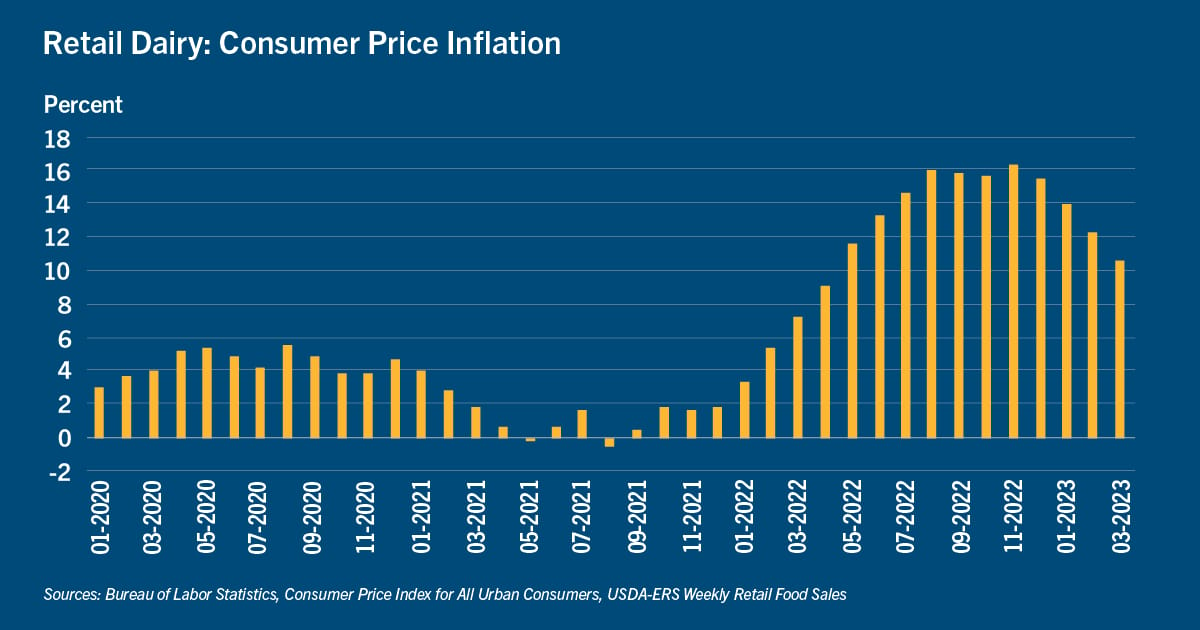

Looking first at the domestic market, which accounts for the vast majority of dairy offtake, consumers remain shell-shocked by food inflation, which has outpaced disposable income gains for 18 straight months. And although broader measures of inflation have eased as of late, food-at-home inflation is still running above 8% annually, and retail dairy case inflation is above 10%. Farmgate commodity prices, including milk, peaked last summer and have been falling ever since — so what’s going on?

The hidden cost of high retail prices

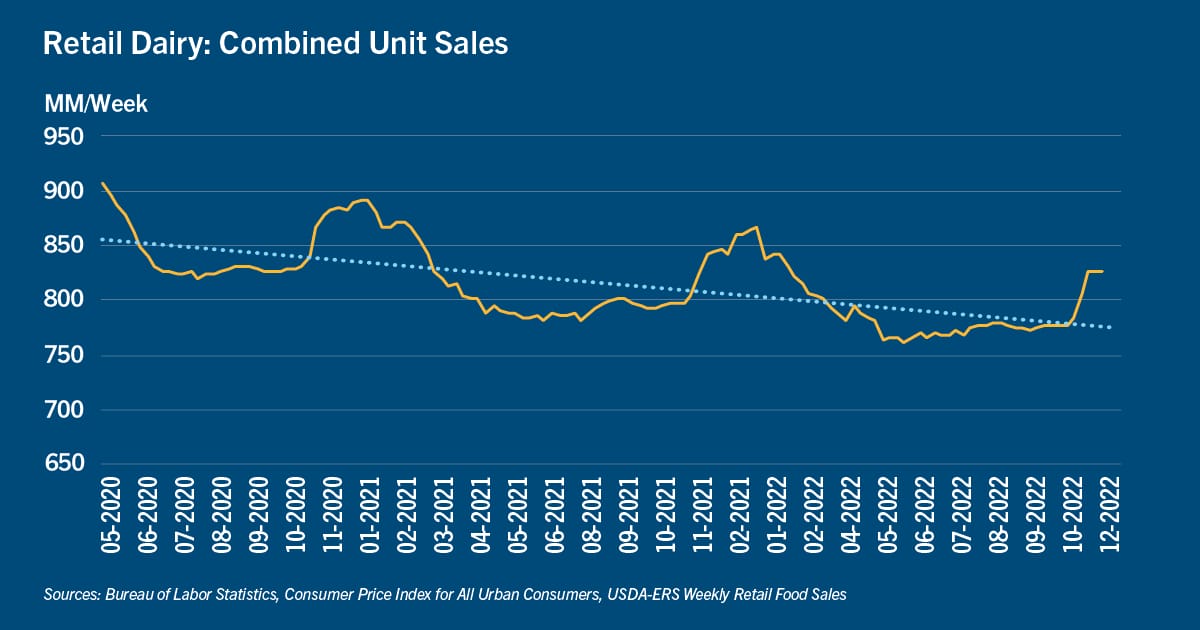

Since the pandemic lockdowns of early 2020, food manufacturers have learned that higher profits are to be found in ever-higher retail prices despite having to put up with modest declines in unit volume sales. And, up until now, that has been the smart choice, but it has unfortunately led to lower consumption of dairy aisle products and consequently put downward pressure on mailbox milk prices for producers. This is one of the reasons that overall U.S. dairy consumption declined 1.1% in 2022 after averaging 1.5% growth over the previous decade, according to the April USDA World Agricultural Supply and Demand Estimates report.

A recent report by the International Dairy Deli Bakery Association, Circana, and 210 Analytics laid bare the facts: For the 52 weeks ending April 2, 2023, price hikes led retail dairy sales to increase 18.3% in dollar value, but unit volume sales to decline 2.4%. USDA’s weekly retail grocery sales data from the beginning of the pandemic through the end of 2022 show that equivalent-volume unit sales (which also account for “shrinkflation” effects) have actually been trending lower since the early stages of the pandemic.

So while consumers have been trying to “push back” on price hikes by buying less, most major publicly traded food manufacturers (including Nestle, Unilever, and Danone) have recently stated that they will continue to hike prices as long as strong profit margins continue.

The cold economic reality of 2023

While consumers have been able to hold their consumption levels reasonably stable thanks to pandemic-era savings, low debt levels, and higher wage rates, economic conditions unfortunately appear to be deteriorating in 2023. GDP growth in the first quarter dropped more than most expected — down to 1.6% vs. 3.7% in the first quarter last year. The other recent red flags of a weakening economy are many and include consumer sentiment, rapidly falling trucking volumes, sharply tightening credit conditions, weaker new home construction, lower manufacturing orders, falling oil prices, a steep drop in ocean container movement, and so on.

Despite all of the above, the U.S. labor market has held up well thus far, but even there we see wage gains now slowing. Most economists believe the full effect of the Fed’s interest rate hikes does not show up in employment numbers for at least 12 months, which means labor markets are just now showing the first responses to the steepest rate hike environment in decades. In other words, we will have to wait another year until we see the story play out. Perhaps the U.S. economy will have the “soft landing” Fed officials are hoping for, but that story seems less and less plausible by the day.

Dairy Export Demand is Weak but Showing Signs of Life

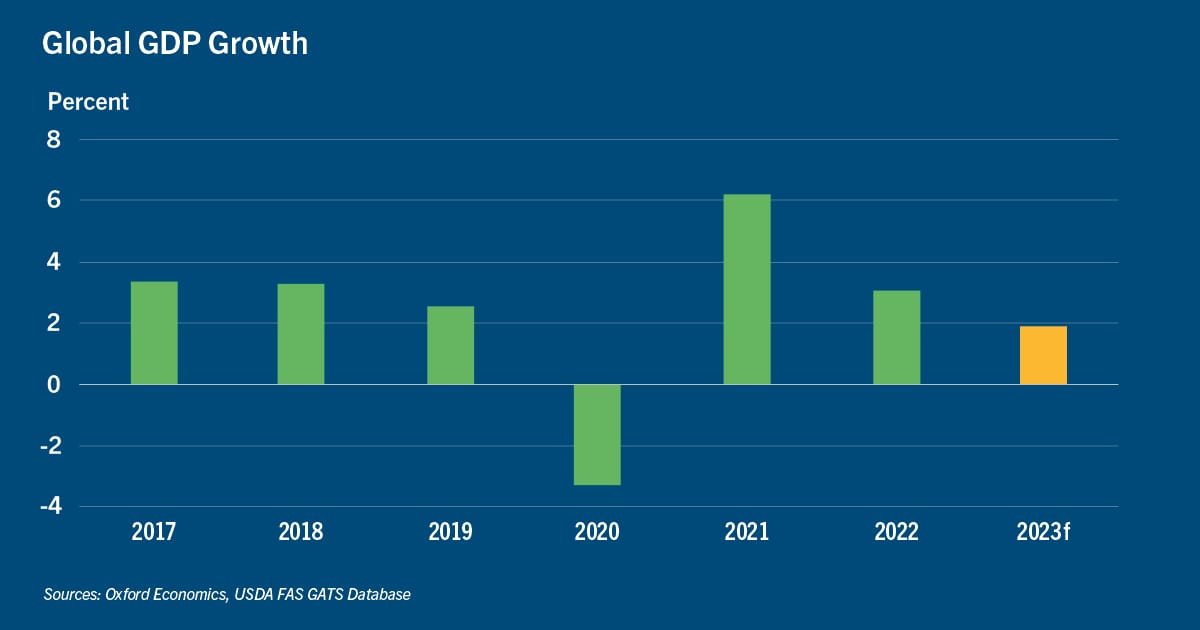

Generally speaking, the global economic outlook does not seem quite as negative. But Oxford Economics, a well-respected economic advisor, is forecasting real global GDP to grow by only 1.9% in 2023, down from 3.1% last year and the lowest non-pandemic yearly pace since 2009. The primary culprits are the relentless monetary tightening policies among central banks and weaker manufacturing expectations in Asia.

Per USDA, after enjoying strong annual growth rates between 2010 and 2019, global imports of both milk powder (skimmed milk power and whole milk power) and cheese have been essentially flat since 2020. The further COVID retreats into the rearview mirror, the more concerning that trend becomes. Over the past two years the U.S. has benefited from lower milk supplies coming out of Europe and New Zealand, which may have somewhat obscured weakening global dairy demand. And while we believe the U.S. will be the primary source of global milk supply growth in the coming decades, it is unwise to discount Europe’s milk production potential during high-price periods.

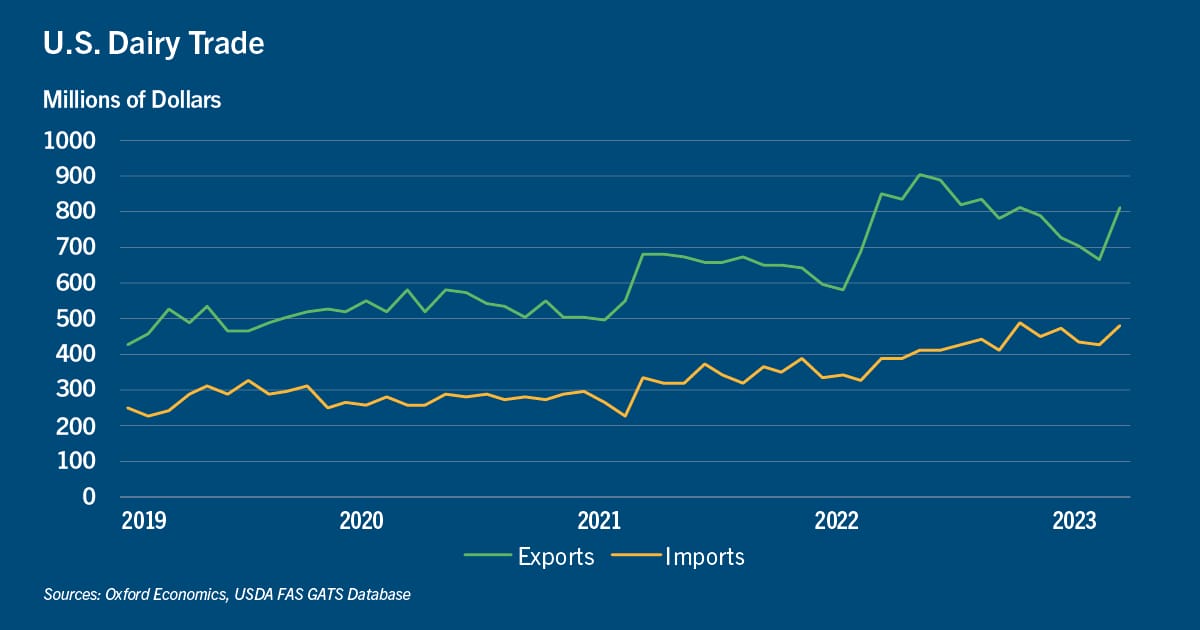

U.S. dairy exports surged in early 2022 but had been trending lower since last May, both on volume and unit price. But the just-released U.S. export numbers for March were big relative to recent months, with across-the-board volume gains by most destinations and many different product categories. Keep in mind that U.S. dairy imports (typically higher-value cheeses, butter, and high protein powders) have also been trending higher over the past two years, so the growth in net dairy trade is not as great as it first appears.

Global Dairy Trade price indexes have been trending lower for the last 12 months. SMP/NDM (skimmed milk power/non-fat dry milk) took the worst of it, falling 40% from the highs of last June. However, prices for all the major categories have come off their lows in recent weeks, which could signal that the bottom has been set and higher prices are on the horizon. So, at least on the export side, things are looking better for dairy demand than they were just a few weeks ago.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.