Chicken wings and breast meat set to offer reprieve for inflation-weary consumers

Brian Earnest

Lower prices of both wing and breast meat in recent months are creating a strong opportunity for grocers and restaurant chains to position chicken as an inflation-busting protein item for consumers. And with March Madness upon us, the timing couldn’t be better.

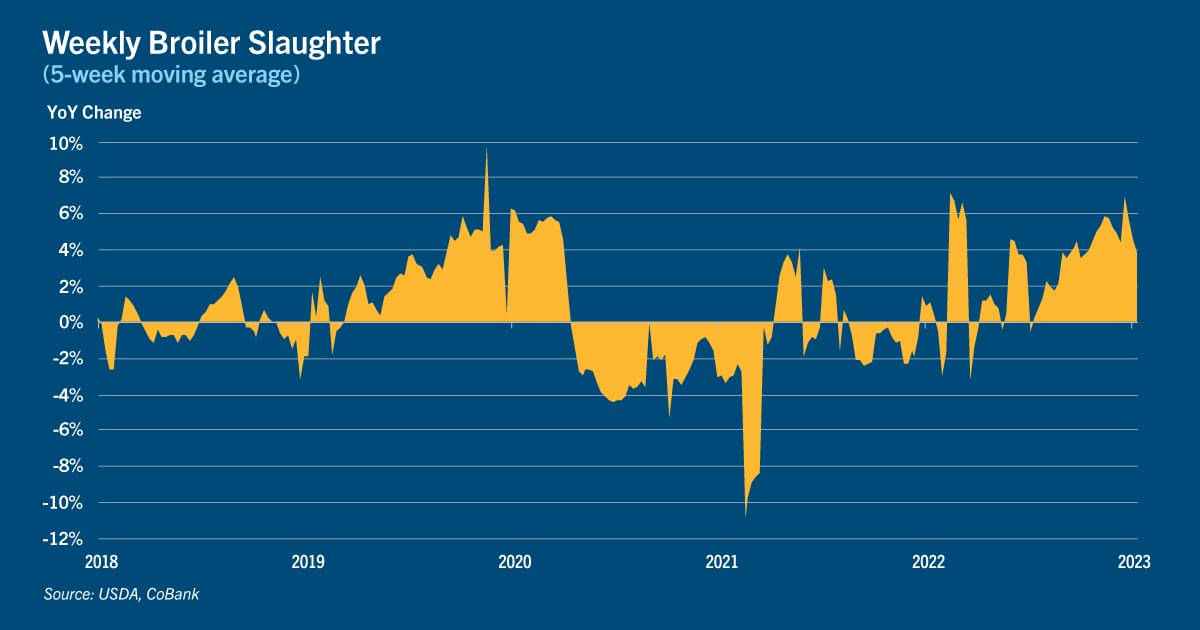

This is welcome news after COVID. Through much of that period, chicken production struggled to keep up with consumer demand for take-out wings, as labor challenges and other supply constraints emerged through 2020 and during the first half of 2021. Weekly slaughter rates went from trending between 4%-6% above year ago levels, to down nearly 4% YoY through late 2020.

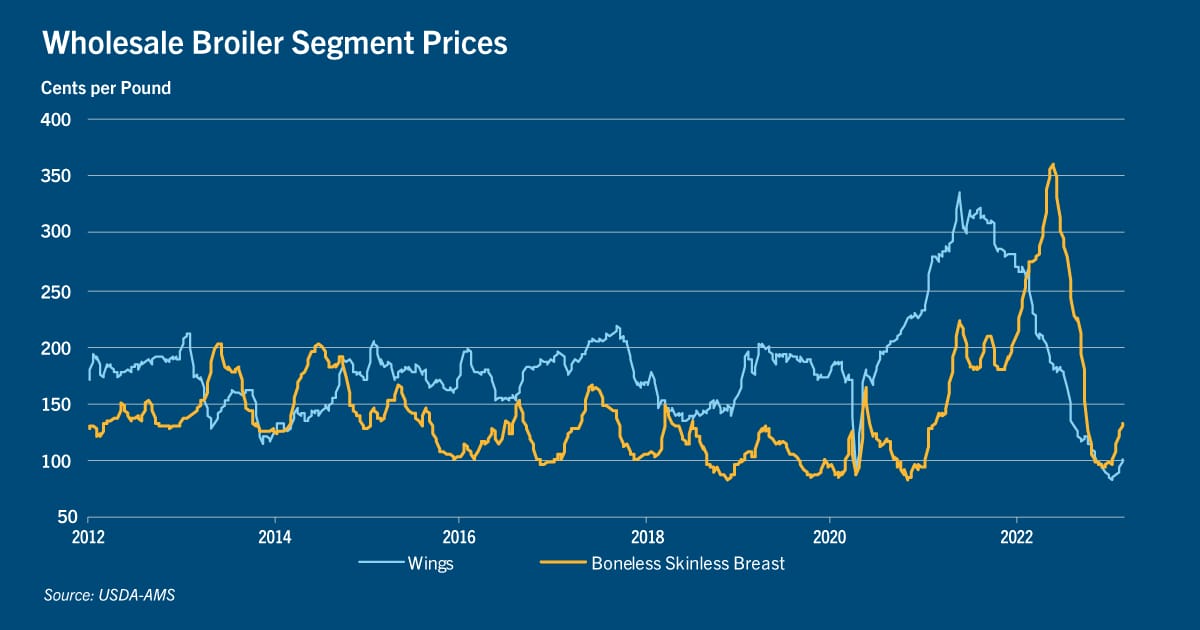

Declining slaughter rates created significant problems for wing supplies in particular, as we’re stuck with the age-old problem of each bird having only two wings. Strong demand coincided with the ongoing supply squeeze, which sent wing prices sky high in 2021.

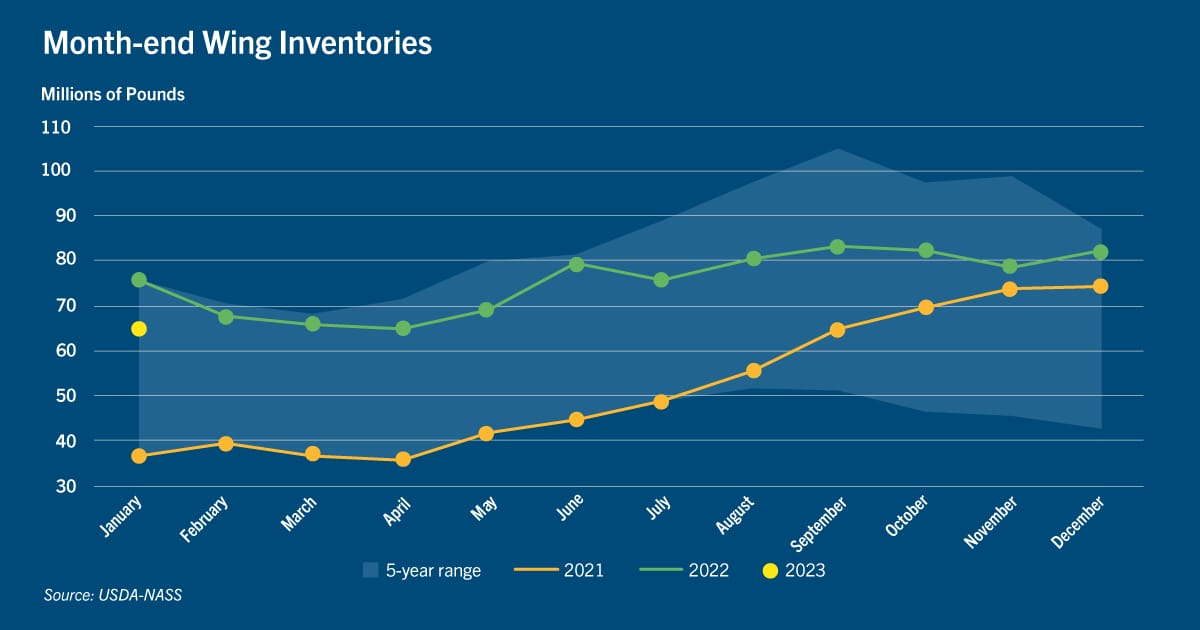

However, when supply began to recover, persistently record-high wing prices proved too much for the market to bear. As a result of market imbalances, wing inventories rose through the end of 2021, and prices began easing during the first quarter of 2022 as needs for the Super Bowl and March Madness (two of the strongest occasion-driven wing disappearance events on the calendar) were fairly easily met.

Wing inventories, as measured by USDA’s monthly Cold Storage reports, went from setting new 5-year lows during 2020 and 2021, to growing to 5-year highs through the first six months of 2022. As they waited for supply recovery, wing-centric restaurants scrambled to divert attention to other offerings. Some wing-only establishments even went as far as marketing drums or introducing chicken sandwiches as alternatives.

During the most recent 12 months, improved line speeds and growth in head count have further eased availability constraints. Through the tail of 2022, the five-week moving average broiler harvest was frequently around 4% above prior year totals. At the same time, live weights have remained at or above trend line, contributing added value on a per-head basis, despite broiler valuation slipping.

Bigger birds helped offset lower slaughter rates

While falling slaughter rates were stressing wing supplies in late 2020, bird weights were eclipsing previous record high levels, often overcoming the deficit in headcount. A good example occurred during the week ended Sept. 9, 2020. Slaughter was short of year ago by 3% but average live weights hit a new record, at 6.48 pounds, helping boost total broiler output 3% YoY. By late 2020, elevated live weights were continually helping to offset lower slaughter numbers – despite lower chick placements as the broiler industry dealt with ongoing breeder problems. Just as wing prices were setting new records, breast meat prices plunged to 20-year lows to end 2020. After finally bottoming out, the market for breast meat garnered attention and gained momentum during the second and third quarters of 2021.

On a tailwind of tighter supplies, high beef prices and resurging food service demand, breast meat prices skyrocketed during the first half of 2022. But production too rebounded – to the tune of an additional 75 million lbs/week on average in the third and fourth quarters, at the very same time disposable incomes were being crunched by inflation and restaurant visits were decelerating. This all sent wholesale chicken markets into freefall by November, which is essentially where markets remain today.

Good news for consumer-facing channels

While this looks bad for chicken producers, it should be very inviting for consumer-facing channels to promote chicken as they prepare for the 2023 grilling season – especially since U.S. beef production is set to hit its lowest level since 2017. With boneless breast meat trending around $1/lb (down from $3.50/lb at mid-year) at the wholesale level to end 2022, it would be surprising if food service and retail outlets alike did not take note and plan accordingly.

This spells price relief for consumers on at least two major animal protein items – chicken wings and breast meat – that they have gravitated towards in recent years, at a time when they are battling inflationary pressures elsewhere.

While market conditions have been favorable for chicken buyers in recent months, the same can’t be said for producers. They have been squeezed by the low chicken prices, but also higher across the board input costs – particularly soybean meal, which has risen 25% over the past three months and is again approaching record highs. Thankfully the strong profitability in 2022 should provide some cushion for chicken producers to weather the current storm of low chicken prices and high feed costs. With the shortage of other proteins and returning demand for chicken, we expect the profitability outlook to improve notably by mid-2023.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.